Why modern founders are no longer building apps around banks they’re building banks inside their apps

A founder once said something during a late-night strategy call that perfectly explained where the fintech industry is heading.

He said, We realized our users didn’t want another banking app. They wanted banking to exist naturally inside the product they were already using.

At first, his company was not trying to become a fintech business at all. They had built a fast-growing digital platform with customers across multiple countries.

The product was doing well, user engagement was strong, and the team was focused entirely on scaling operations. But over time, one issue kept appearing again and again. Customers constantly had to leave the platform to complete financial actions somewhere else.

Payments happened externally. Payouts were delayed because of traditional banks. International transfers were slow. Users needed separate wallets, separate banking apps, and separate financial tools just to complete basic transactions.

Every extra step created friction.

And friction quietly kills growth.

That was the moment the company started exploring Banking-as-a-Service, commonly known as BaaS.

Like many founders initially, they assumed banking infrastructure was something only licensed banks could build. The idea of offering financial services inside their own platform sounded expensive, complicated, and nearly impossible.

They imagined years of regulatory approvals, banking partnerships, compliance teams, and massive engineering costs before they could even launch a single financial feature.

made by ai

But what they discovered completely changed their perspective.

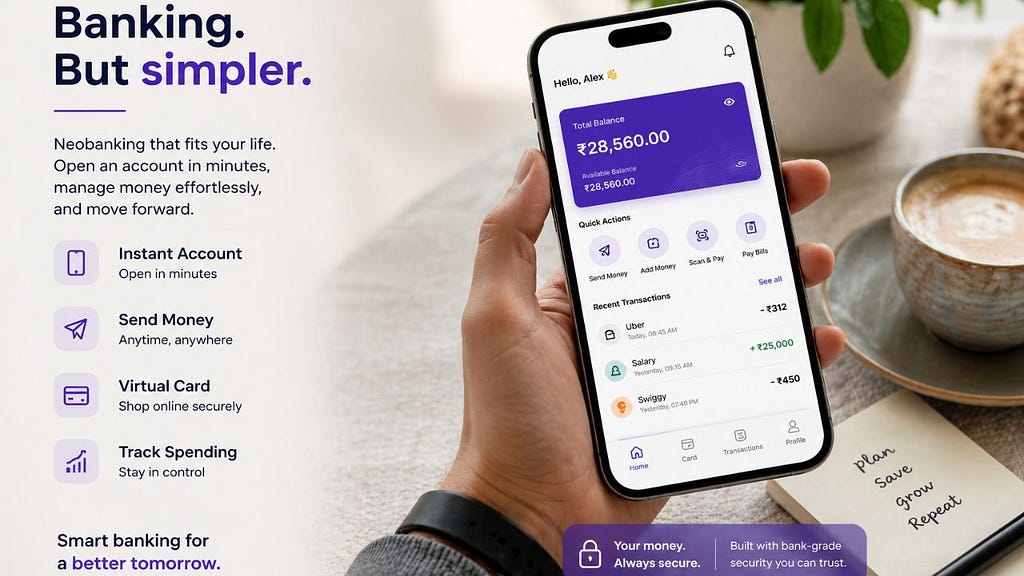

Banking-as-a-Service allows businesses to integrate real banking capabilities directly into their platforms without becoming a traditional bank themselves.

Through BaaS infrastructure, companies can offer services like IBAN accounts, virtual wallets, card issuing, international payments, SWIFT access, real-time transfers, multi-currency accounts, and embedded finance experiences all under their own brand.

To the customer, it feels seamless.

The financial experience becomes part of the product itself and that changes everything.

What most people fail to realize is that modern customers no longer separate banking from digital experience. Users expect financial functionality to exist wherever they already spend time.

They want platforms to move money instantly, issue cards immediately, handle cross-border transactions smoothly, and simplify financial management without forcing them into traditional banking systems.

This is exactly why Banking-as-a-Service has become one of the most important shifts in modern fintech.

It is not just changing how banking works. It is changing who gets to offer banking.

For decades, financial infrastructure was controlled almost entirely by large institutions with massive regulatory barriers protecting the industry. Startups could build apps around banking, but they rarely controlled the actual infrastructure. BaaS changed that model completely by opening banking capabilities through APIs and scalable infrastructure partnerships.

Now, almost any ambitious company can integrate financial services directly into its ecosystem.

And founders are beginning to understand how powerful that really is.

The first major advantage is customer retention. The more financial activity happens inside a platform, the more valuable the ecosystem becomes to users. Instead of customers leaving your app to complete transactions elsewhere, everything happens inside your own environment. Payments, wallets, cards, transfers, and financial interactions all become part of the core user experience.

The second advantage is speed. Building banking infrastructure from scratch would normally take years of licensing, compliance approvals, engineering resources, and banking negotiations. Most startups simply do not have the time, capital, or operational capacity for that journey. Banking-as-a-Service compresses that timeline dramatically by providing ready-made infrastructure businesses can integrate much faster.

That speed allows founders to focus on growth instead of rebuilding financial systems from zero.

Then comes scalability, as companies expand globally, financial complexity increases rapidly. Businesses suddenly need multi-currency support, cross-border settlement systems, regulatory frameworks, local payment rails, card programs, and compliance structures across multiple jurisdictions. Without strong infrastructure, international expansion becomes extremely difficult.

BaaS simplifies much of that complexity by providing scalable financial rails businesses can build on top of.

We work with fintechs, digital banks, and ambitious founders who want to launch globally scalable financial infrastructure without spending years navigating the traditional banking system alone.

Through Banking-as-a-Service, embedded finance, IBAN accounts, SWIFT connectivity, wallets, card issuing, real-time payment rails, white-label payment gateways, crypto infrastructure, and compliance-ready systems, founders are able to launch sophisticated financial products in weeks instead of years.

But what makes Banking-as-a-Service truly important is not just the technology itself.

It is what the technology allows businesses to become.

A logistics company can suddenly offer financial services to drivers. An e-commerce platform can provide merchant wallets and payouts. A SaaS business can embed payments directly into workflows. A global startup can operate across borders with multi-currency infrastructure built into the platform from day one.

In other words, banking is no longer limited to banks.

And that is one of the biggest shifts happening in the digital economy right now.

The companies that understand this early are building entirely different kinds of businesses. They are creating ecosystems instead of standalone products. They are increasing customer loyalty, controlling more of the financial experience, unlocking new revenue streams, and reducing dependency on outdated financial systems.

Most users may never notice the infrastructure behind the scenes.

They will simply experience faster transactions, smoother payments, instant wallets, and seamless financial interactions.

But founders understand something much bigger is happening underneath.

The future of banking is no longer about where people bank. It is about where banking quietly appears.

The Biggest Shift in Fintech Isn’t Crypto or AI. It’s Banking as a Service. was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.