The Biggest Fintech Myth Holding Businesses Back: You Don’t Need to Be a Bank to Offer Banking Services

Modern financial infrastructure has changed the rules. Today, fintechs, SaaS platforms, marketplaces, and digital businesses can deliver banking experiences without becoming banks provided they partner with the right licensed infrastructure.

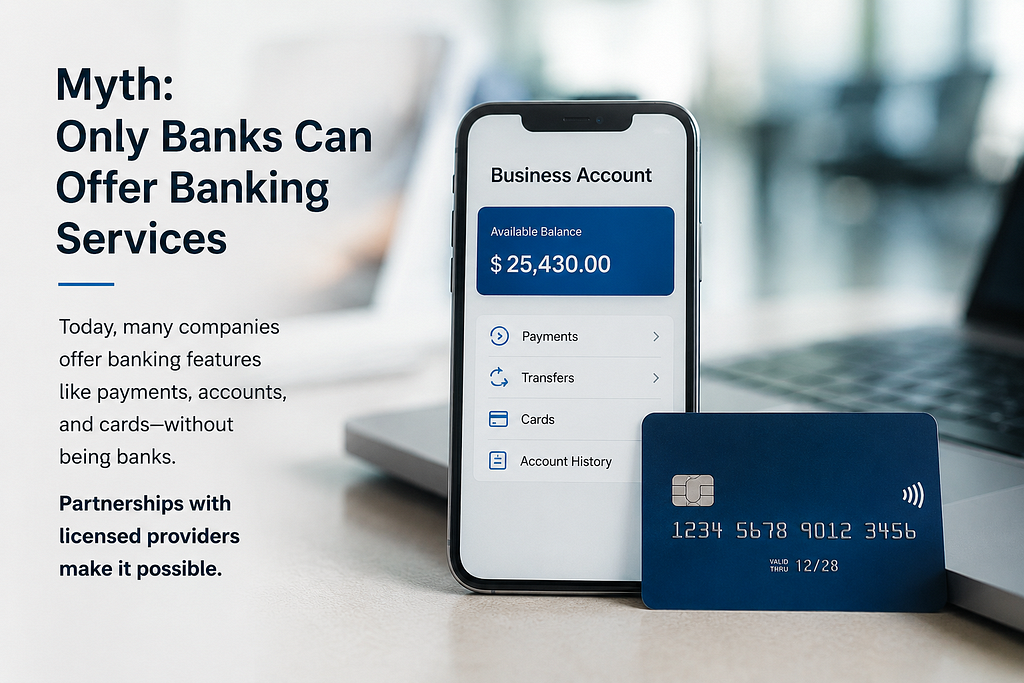

For decades, there was only one generally undisputed rule about the financial industry, if you want to provide banking services, you have to open a bank.

Banking licenses, compliance departments, hundreds of regulators, and billions in capital were some of the high barriers to entry that only large multinational conglomerates could overcome

That belief, however, is now an outdated perspective that does not take into account recent innovations in the financial industry. Namely, many financial institutions now rely on specialized enablers to provide regulated banking-like services to their clients.

As such, the banking-as-a-service (BaaS) economy now enables non-financial institutions to embed payments, wallets, cards, accounts, and other financial services and functions within their own P2P and B2B commerce platforms, apps, and sites

This new industry trend ultimately results in a situation where the line between technology and finance gets blurred, often to the point where neither one is particularly obvious to the consumer

The new BaaS economy disrupts the traditional financial services industry in numerous ways, from allowing non-banks to embed financial services inside their platforms to enabling technology companies to innovate and specialize in different aspects of the financial value chain

The most basic characteristic of the BaaS economy is that it enables collaboration between financial institutions that hold banking licenses and technology companies that operate as enablers. The former provides the backbone services and products, such as custodian accounts and deposits,

While the latter embed them in their platforms to facilitate everyday P2P and B2B payments, money transfers, issuing cards, lending, and other financial services

The overall purpose of BaaS is to separate the core banking infrastructure from the front-end technologies and make it much easier for companies to adopt and customize financial services, rather than having to build them from scratch.

The BaaS economy ultimately makes a wide variety of financial services accessible to a much broader audience of innovators and entrepreneurs. Some examples of such companies include technology-native financial platforms that embed cards and accounts as a way to make their business-to-business and business-to-consumer transactions more efficient, secure, and transparent

For example, many of the largest technology companies today offer their business clients an option to open business accounts and receive payments directly through their digital platforms.

In that way, BaaS ultimately empowers the technology industry to disrupt the financial services industry by embedding financial infrastructure as a way to improve products and services offered by non-financial companies.

At the same time, the BaaS economy is not removing the importance of financial institutions, as they remain critical enablers of the digital economy.

A fundamental change brought by the BaaS economy is that it focuses on the needs of the consumer. Embedded finance ultimately puts the consumer at the center of the financial experience, which means the overall experience has to be much more intuitive and more compelling

The BaaS economy therefore ultimately shifts the paradigm to create value by complementing existing products and services with financial services and functions

The opportunities for such financial complementarities are countless, as they can be found in virtually every industry and every company, regardless of their size or specialization.

An e-commerce marketplace can allow its merchants to receive instant settlements, rather than having to wait for several days for the money to clear. A payroll company can allow its workers to open mobile accounts and receive payments instantly, as well as issue cards that can be used to make purchases.

A logistics company can make it much easier for its business clients to settle international payments, while a SaaS company can allow its clients to send and receive money directly through the SaaS platform. In each of these examples, the financial infrastructure enhances the core vertical, which ultimately results in a much better client experience.

Ultimately, the embedded finance model can be seen as much more efficient and effective way to distribute financial services, as it ultimately makes them more accessible and easier to use.

It is important to note that financial regulations have not gone away, despite the rapid rise of the BaaS economy. Financial services have always been one of the most heavily regulated industries worldwide, and they continue to be subject to extremely strict anti-money laundering (AML), compliance, transaction monitoring, and data privacy regulations.

However, many of those regulations can now be handled by BaaS enablers (i.e., financial institutions that specialize in reselling their infrastructure and technology to other companies). Such enablers handle the banking license, custodian accounts, deposits, transaction clearing, and other aspects that were traditionally the responsibility of the financial institutions that provided those services directly to the consumer

Therefore, the BaaS economy ultimately lowers the regulatory barriers for non-financial companies that want to embed financial services within their platforms and products. At the same time, the BaaS economy also reduces the implementation costs and the amount of time needed to launch new financial products and services

That is especially important for smaller technology companies and start-ups that would not be able to launch a financial services product, even if they wanted to, due to the immense costs involved. It takes hundreds if not thousands of employees for technology-native financial platforms to manage risk, comply with regulations, maintain the necessary IT infrastructure, and provide excellent consumer support.

By collaborating with BaaS enablers, such companies can significantly reduce their costs and risks by relying on the expertise of financial infrastructure providers and their extensive regulatory experience.

The BaaS economy ultimately lowers the barriers to entry for everyone involved. New entrants can launch more innovative financial products and services with reduced risk and cost.

Simultaneously, larger financial services companies can use the BaaS economy to scale their operations faster by relying on the business-to-business (B2B) infrastructure provided by technology enablers. At the same time, the widespread adoption of the BaaS economy allows even non-financial and non-technology companies to embed wallets and payments solutions within their business-to-consumer (B2C) and business-to-business (B2B) operations.

Such opportunities ultimately allow diverse sets of companies to compete more effectively while improving products and services offered to their consumers.

One of the reasons why the BaaS economy is misunderstood is because some of the most basic principles have not been fully acknowledged. The banking industry has long held the belief that only banks can offer banking services.

Yet, in the twenty-first century, the most valuable financial services innovations are being driven by companies that are not financial institutions, even if they collaborate with banks and other financial institutions.

There is nothing mysterious or counterintuitive about this trend the banking-as-a-service economy ultimately reflects the fact that the finance industry has started to behave like any other technology-driven industry.

Just like many other technologies, finance is now being unbundled between different specialized enablers, each of which plays a specific role in the client experience. The core infrastructure remains the domain of financial institutions, while the front-end technology is now being developed by companies that care to customize the financial experience for their clients.

By enabling those enablers, the BaaS economy ultimately promotes competition, lowers the costs and complexity of financial services, and provides those services to a much broader audience.

The finance industry no longer has a duopoly between large technology companies and big banks, with the competition between the two often stifling the innovation at the intersection between the two domains. Instead, the BaaS economy enables a much more dynamic and diverse financial services ecosystem that ultimately benefits everyone involved.

Perhaps the most important insight regarding the BaaS economy and the embedded finance space is that the entire financial services industry will ultimately become dominated by non-bank enablers that embed financial services within their products and technologies.

This development is ultimately driven by the demand for convenience and ease of use, as consumers are much more likely to use financial services when they do not have to deal with the hassles and complexities of the traditional finance industry.

The BaaS economy ultimately recognizes that the most valuable financial services are the ones that are embedded within other technology products and services. As such, the future of financial services is no longer dictated by banks, but rather the companies and platforms that utilize banks’ infrastructure to create compelling financial products for their clients.

The Biggest Fintech Myth Holding Businesses Back: You Don’t Need to Be a Bank to Offer Banking… was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.