Why the next generation of fintech, SaaS, marketplaces, and digital platforms will be built on embedded financial infrastructure

By 2026, startup creators aren’t pausing to debate if fintech features belong in their offerings. Instead, they’re moving straight into setup. Decisions once filled with doubt now feel automatic. The hesitation has faded. What used to spark long talks is now just part of the plan. Questions about inclusion have lost their weight. Building without finance tools seems odd now. Momentum has shifted beneath them. Choice isn’t really a choice anymore.

How fast can they get it done? That’s what people keep wondering.

Here’s why things are shifting people now assume money tools fit right into the apps they open every day. Not just sometimes, but always there, like a built-in feature rather than an extra step. Payments show up inside shopping tabs. Wallets live alongside transit passes. Cards get managed without switching screens. Lending appears when budgets tighten. Even sending cash abroad feels seamless within chat threads. One spot holds it all not scattered across separate sites.

Out of nowhere, BaaS has become a key force behind startup expansion in banking tech. Suddenly, digital companies rely on it more than ever to grow fast. Because systems now plug directly into financial infrastructure, new players find their footing quicker. Where older models hesitated, these services leap ahead. Growth isn’t just easier it’s reshaped from the ground up.

What Is Banking-as-a-Service?

Banking-as-a-Service allows non-bank companies to embed regulated financial products directly into their platforms through APIs.

Founders might skip building a bank by tapping into existing licensed platforms that support financial offerings like these:

Virtual and physical debit cardsMulti-currency accountsIBAN accountsDigital walletsPayment processingCross-border transfersLending productsCompliance and KYC onboarding

A fintech startup, an e-commerce site, a SaaS business, or even a marketplace each might roll out financial services fast, bypassing the long grind of securing bank licenses. Instead of wrestling with heavy tech systems, they move quickly, using ready solutions behind the scenes.

Baas gain importance in 2026

A fresh chapter begins for financial technology. New shapes appear in how money tools evolve. Changes ripple through the sector quietly. This moment shifts what comes next without warning.

Digitization of banking took center stage at first. Fueled by new tech, the second push shook up old banking systems. Finance sneaking into everything marks what’s unfolding today. Right in this moment, it slips into corners you might not expect.

Built right into the apps people use every day, financial tools now work without being seen. Where you shop, chat, or browse money moves quietly in the background. Hidden but always active, they show up exactly when needed. Not a separate step, just part of how things function now. Running beneath the surface, finance blends into daily actions.

Those building companies today might see clearer paths forward if they notice what’s changing. Early recognition could separate the ones who adapt from those left behind.

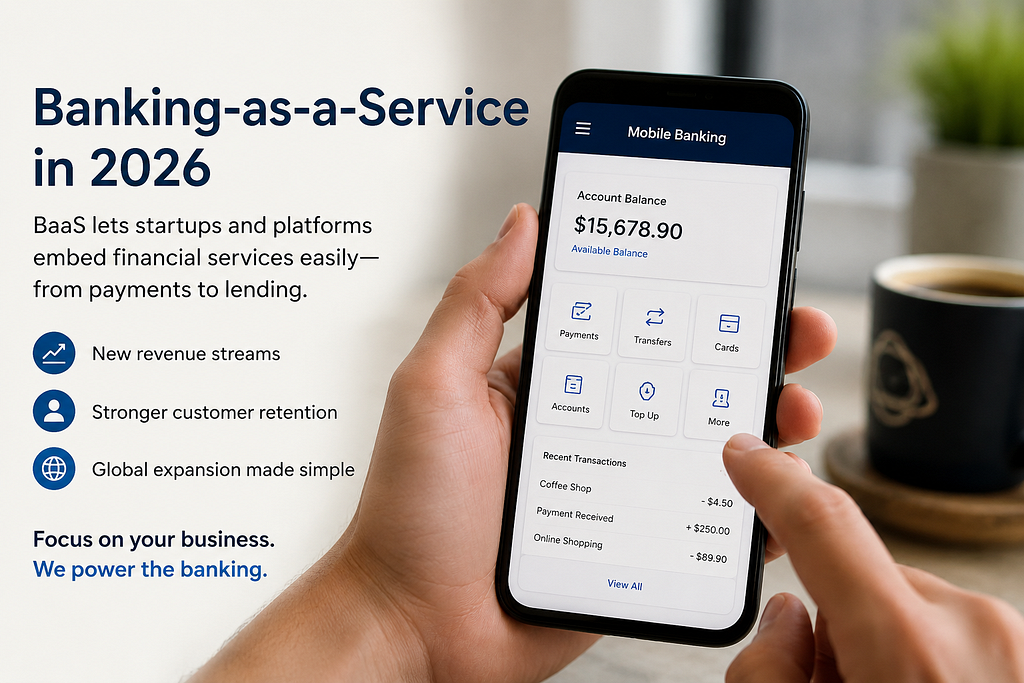

New Revenue Streams Without Building a Bank

Finding ways to make money often trips up those starting a business. It’s not always clear how income should flow when building something new.

These days, just relying on subscription income feels tighter when it takes more money to bring each new person in. Rising costs shape how far that model can stretch.

BaaS opens entirely new revenue opportunities:

Card interchange revenuePayment processing feesForeign exchange marginsLending commissionsWallet transaction feesPremium financial services

Founders who spread their income across different streams often see stronger returns over time. One path alone might limit growth, yet mixing approaches opens more doors. Customers tend to stay longer when offerings adapt. Relying only on one method? That tightens margins. Trying varied ways builds resilience quietly.

Beyond a simple add-on, some young companies now earn real income through built-in financial tools. Profit streams emerge where services once only supported core offerings.

Customer retention improves

Most people stick with one app for handling cash. Rarely do they jump to another option once settled in place.

Becoming the spot where people keep money often leads to more activity. Payments flowing through it pull users back again and again. Payouts arriving there create routine check-ins. Handling day-to-day spending ties them closer over time.

Once focused on software alone, a company might grow into a vital money-handling center for customers. Now handling payments, it connects deeply with daily operations. Its tools shift from optional extras to essential backbones. Where code used to rule, trust now matters more. Stability emerges where flexibility once led. Users rely less on features, more on function. Not just a product anymore, it anchors routines.

The result?

Sticking around longer means fewer people leave. Fewer exits open space for stronger bonds to form. Relationships grow when time spent together increases.

Global expansion now more accessible

Global from day one, that’s how most new businesses begin by 2026.

A startup creator based in Europe could reach buyers across Africa right away, also touching Southeast Asia, then the Middle East, all while connecting with people in North America early on.

Banking-as-a-Service providers now offer:

Multi-currency capabilitiesInternational payment railsGlobal card issuanceCross-border settlementCompliance support across jurisdictions

Founders can grow across borders now because they won’t need a new bank in each country. Banking hurdles fade when one system works everywhere at once.

The Rise of Embedded Finance

One app per money task feels outdated now. People skip juggling separate tools just to manage cash. Handling finances means fewer taps, not more screens. A single place beats a pile of icons today. Simplicity wins where clutter once ruled.

They expect:

Ride-sharing apps with walletsMarketplaces with instant payoutsSaaS platforms with integrated paymentsCreator platforms with banking featuresE-commerce platforms with financing options

Some companies offering such experiences notice better interaction numbers along with improved market standing.

Come 2026, baked-in financial services just blend in. They don’t stand out anymore. People now assume it will happen.

Regulatory complexity no longer stops progress

Back then, rules around money matters kept most new businesses out of finance work.

Today, modern BaaS providers help businesses navigate:

Checking who you are plus stopping dirty money rulesPCI DSS complianceData protection regulationsRisk management frameworksLicensing partnerships

Founders spend less time managing daily tasks, which leaves more room to build their product and bring in users instead. Yet staying on top of operations becomes simpler when energy shifts toward what customers need most.

AI and Banking as a Service Combined Create New Possibilities

Artificial intelligence is transforming financial services.

Founders might build tailored money tools when they team up with Banking-as-a-Service offerings

Smart spending insightsAutomated budgetingPersonalized lending decisionsPredictive cash-flow managementAI-powered fraud detection

Few fintechs launch in the coming years will stand out like those built on smart software woven into financial systems. A quiet shift happens when machines learn patterns while services run beneath the surface. Success hides where learning code meets hidden bank networks. Most breakthroughs won’t shout they’ll simply work better, shaped by unseen layers talking to each other. Hidden intelligence paired with deep integration drives what comes next.

Final Thoughts

Fresh off the back of tech shifts, Banking-as-a-Service now runs quietly beneath most digital ventures. While apps change fast, this layer stays steady powering transactions without fanfare. Behind sleek interfaces, it handles money moves like an unseen engine. Not loud, yet everywhere. As business models twist and turn, they lean on it more each day.

Founders now assume money tools come baked into what they build. It’s a given, not a debate, Will rivals beat them to it? That’s what matters.

One step ahead, firms using BaaS by 2026 start pulling income from fresh directions. Retention climbs when customers feel anchored through better service loops. Global reach stretches faster than expected thanks to modular setups. Product worlds grow thicker, tied together by shared access points instead of loose partnerships.

The next generation of billion-dollar companies may not look like banks. Yet out of view, most rely on systems built by banks.

Banking as a Service in 2026: The Infrastructure Every Founder Will Wish They Started With was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.