I. Executive Summary

This article looks at how Chainlink has developed from a decentralized oracle network built mainly for DeFi into a more established piece of infrastructure that traditional financial institutions are starting to use as they explore tokenized assets. It begins by explaining the oracle problem, which is the difficulty blockchains face in securely accessing information from the outside world, and how Chainlink was created to solve it through decentralized data delivery and cross-chain communication.

The article goes through Chainlink’s main services, including Data Feeds, Data Streams, CCIP, Proof of Reserve, NAVLink, and the Chainlink Runtime Environment. It shows how these tools work together to support real institutional use cases such as tokenized funds, cross-chain settlement, and automated processes.

A large part of the discussion focuses on Chainlink’s token economics. The introduction of Payment Abstraction and the Chainlink Reserve in 2025 marks a shift toward capturing actual network revenue and directing some of it back into LINK. While the network is still inflationary due to ongoing token unlocks, these changes improve the connection between real usage and long-term token value.

The article also examines the wider tokenization opportunity. Although the current market for tokenized real-world assets is still relatively small, forecasts from major research firms suggest it could grow significantly over the next several years. It reviews Chainlink’s involvement in several institutional projects, including work with JPMorgan, DTCC, SWIFT, and various asset managers.

In terms of competition, the article notes that while Pyth and RedStone have made progress in certain areas, Chainlink continues to hold a strong position in more complex institutional environments. Overall, the analysis suggests that Chainlink is well placed to benefit from further progress in tokenization, though the speed of its revenue growth will depend on how quickly institutions move these assets into actual production use.

II. The Oracle Problem and Chainlink’s Origin

One of the most persistent and underestimated limitations of blockchain technology is the “oracle problem.” In simple terms, blockchains are self-contained, deterministic systems. They excel at verifying transactions and executing code among participants who already agree on the rules, but they have no native ability to securely retrieve or verify information that originates outside their own network. This creates a fundamental gap: how can a smart contract know the current price of Apple stock, the outcome of a sports match, the balance in a bank account, or whether a real-world asset is properly collateralized?

Without trustworthy external data, smart contracts are limited to operating only on information that already exists on-chain. This severely restricts their usefulness for real-world applications such as decentralized finance (DeFi), insurance, supply-chain tracking, or tokenized real-world assets (RWAs). A smart contract cannot reliably pay out on a weather-derivative contract, settle a prediction market, or verify that a tokenized Treasury bond is backed 1:1 by actual government securities unless it can securely import that external truth. Early attempts to solve this relied on centralized data providers or trusted third parties, which reintroduced single points of failure and undermined the core promise of decentralization.

The oracle problem has been widely recognized in academic and industry literature. In 2016, researchers at Cornell University described the lack of a substantive ecosystem of trustworthy data feeds (oracles) as a frequently cited “critical obstacle” to the evolution of Ethereum and decentralized smart contracts in general, because they represent a key trust bottleneck between the on-chain and off-chain worlds. [1]

Chainlink was founded specifically to solve this problem. In September 2017, Sergey Nazarov and his co-founder Steve Ellis launched SmartContract.com, the company that would later become Chainlink. Nazarov had been thinking about the oracle challenge since at least 2014, when he observed that blockchains were excellent at consensus and execution but fundamentally blind to external reality. His insight was that a decentralized network of independent nodes could collectively fetch, validate, and deliver off-chain data to smart contracts in a tamper-resistant way, using economic incentives and cryptographic proofs rather than blind trust in a single provider.

The original Chainlink whitepaper laid out a vision for a decentralized oracle network that could support any type of data or computation while remaining secure and scalable. [2] The core innovation was a reputation-and-staking-based system in which node operators are incentivized to provide accurate data, with penalties (slashing) for misbehavior. This design allowed Chainlink to start as a price-feed oracle for early DeFi protocols on Ethereum and gradually expand into a full-suite infrastructure layer.

By 2019–2020, Chainlink had become the dominant oracle solution in DeFi. After launching its mainnet in May 2019, it quickly secured integrations with leading protocols such as Synthetix, Aave, and Compound. Contemporary reporting from that period described Chainlink as having “dominated the oracle space” and taken a “commanding lead among DeFi oracles.” [3] This early dominance was driven by the explosive growth of decentralized lending and derivatives, which required reliable, decentralized price oracles. Chainlink’s approach, aggregating data from multiple independent sources and publishing it on-chain with cryptographic proofs, addressed the concrete risks of outages, manipulation, and stale data that plagued earlier centralized oracle designs.

However, the real transformation began in 2024–2025. As institutional interest in tokenized real-world assets accelerated, Chainlink evolved from a DeFi tool into critical infrastructure for TradFi. The launch of Payment Abstraction and the Chainlink Reserve in August 2025 marked a pivotal shift: fees from high-value services began flowing automatically into an on-chain strategic reserve that buys and locks LINK, creating a direct link between real-world usage and token economics.

Today, Chainlink is no longer just an oracle for crypto-native applications. It has become the secure bridge that large institutions rely on when they want to move tokenized assets between permissioned networks and public blockchains, or when they need verifiable real-world data inside smart contracts. This evolution from a niche DeFi solution to a foundational layer for institutional tokenization is what makes Chainlink one of the most strategically important projects in the entire crypto ecosystem.

Oracle Necessity in Tokenized Assets

Even in permissioned blockchains built specifically for institutions, such as the Canton Network or JPMorgan’s Kinexys platform, the need for external data does not disappear. These networks are designed with privacy, compliance, and controlled participation in mind, yet they still operate in a closed environment that cannot natively access real-world information.

To deliver meaningful utility, tokenized assets on these platforms require oracles for several critical functions. Accurate net asset value calculations, Proof of Reserve attestations, corporate actions processing such as dividends, splits, and redemptions, and programmable features like automated collateral management or dynamic yield all depend on secure external data. Without oracles, institutions cannot reliably use tokenized Treasuries or funds as collateral, settle cross-chain trades, or provide the transparency that global investors demand.

There is a clear distinction between fully on-chain models and hybrid legal models. In a fully on-chain model, every aspect of the asset, including ownership, valuation, corporate actions, and settlement, lives entirely on the blockchain. In practice, most institutional tokenization today follows a hybrid legal model. [4] Legal ownership and regulatory compliance remain in traditional systems such as custody accounts and prospectuses, while the blockchain handles issuance, transfer, and programmability. In these hybrid setups, oracles serve as the essential bridge that keeps the on-chain representation synchronized with off-chain reality.

Oracles are not always required. In very simple, static use cases such as a basic ownership token that only records who holds a property deed or government bond, the blockchain can function without external data. In these cases, the issuing institution or government registry itself serves as the single source of truth, so oracles are not strictly necessary at this stage.

However, as soon as institutions or governments want to move beyond basic digital records and make tokenized assets globally interoperable and liquid, external data becomes essential. For example, when these assets need to be used as collateral in external lending protocols, traded across different blockchains, or trigger automatic liquidations based on real-time market prices, oracles are required. For credibility with global institutions and major international banks, independent verification is critical. Proof-of-reserve attestations, independent NAV calculations, and fund-level metrics must come from trusted external sources that go beyond any single institution or government system. This is precisely why even the most sophisticated permissioned networks, including Canton and Kinexys, have actively integrated oracles.

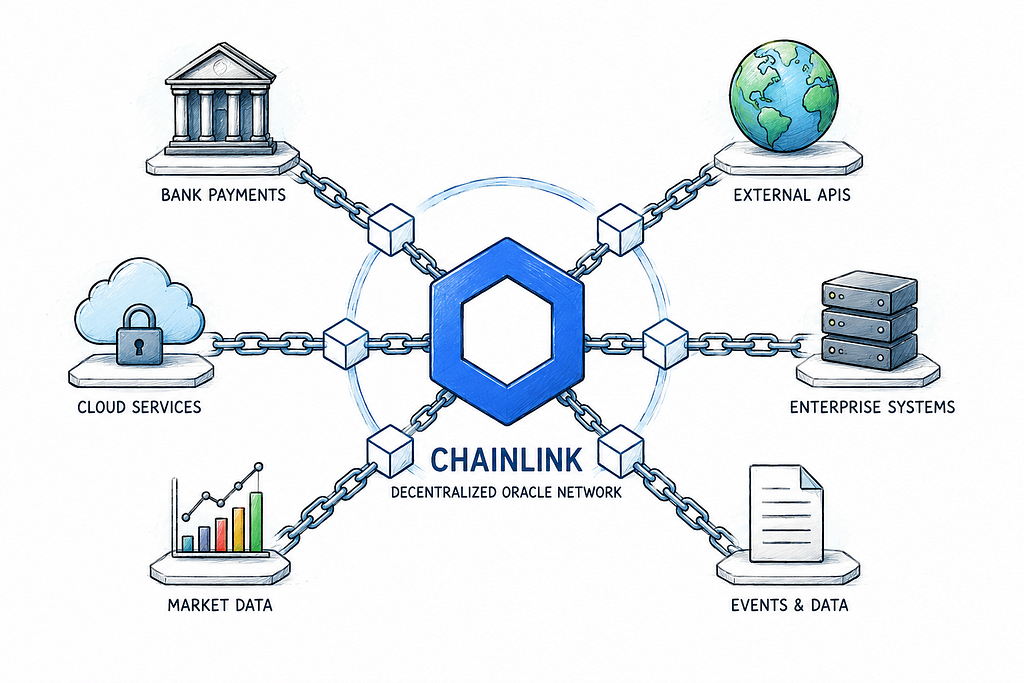

III. Chainlink’s Service Portfolio: Technical Overview

Chainlink is not a single product but a suite of decentralized services designed to solve different aspects of the oracle problem. Each service addresses a specific need that arises when smart contracts must interact with the outside world. What makes Chainlink unique is that these services are built to work together, creating a comprehensive infrastructure layer that institutions can use whether they are operating on public blockchains, permissioned networks like Canton, or hybrid setups.

Below is a detailed explanation of every major Chainlink service, including how it works and real-world examples of its adoption.

1) Data Feeds

Chainlink Data Feeds are the original and still most widely used service in the Chainlink suite. They provide smart contracts with decentralized, tamper-proof price and market data for assets ranging from cryptocurrencies and fiat currencies to stocks, commodities, and indices.

Technically, multiple independent node operators fetch data from various premium and public sources, aggregate it using a median or weighted average, and publish a signed, on-chain value that smart contracts can read. This design prevents any single point of failure or manipulation. [5]

Real-world use: Chainlink Data Feeds currently secure 58% of all Total Value Secured (TVS) across DeFi protocols on Ethereum, Solana, and other chains, making them the dominant price oracle in decentralized finance. The second-largest oracle, Chronicle, holds approximately 13% of the TVS market. [6] They are used for critical functions such as collateral valuation, liquidations, and trading in major protocols.

2) Data Streams

Chainlink Data Streams, launched in 2024 and significantly expanded in 2025, delivers ultra-low-latency, high-frequency market data. While standard Data Feeds update every few minutes, Data Streams can deliver signed price updates in milliseconds with cryptographic signatures that smart contracts can verify instantly. [7]

This service is particularly valuable for high-performance applications such as perpetual futures, options, and real-time trading strategies that were previously difficult to run fully on-chain.

Real-world use: Polymarket, one of the fastest-growing prediction market platforms, uses Chainlink Data Streams for many of its high-volume crypto price prediction markets. [8] This integration enables near-instant, dispute-free settlement. Polymarket experienced explosive growth in 2025 and 2026, with total monthly trading volume surpassing $11 billion. [9] The same low-latency capabilities are increasingly important for tokenized equities. Platforms like Backed (xStocks), which powers tokenized versions of major U.S. stocks and ETFs such as AAPL, TSLA, and NVDA, rely on Chainlink Data Streams for real-time, 24/5 pricing and risk management. These tokenized stocks are actively traded on Kraken, Bybit, and Solana DeFi platforms, where accurate, high-frequency price data is essential for liquidity and collateral use. [10]

3) CCIP (Cross-Chain Interoperability Protocol)

CCIP is Chainlink’s flagship cross-chain messaging and token transfer service. In simple terms, it acts as a secure, decentralized bridge that enables smart contracts, and traditional financial institutions, to communicate and transfer assets across different blockchain networks. This includes public chains such as Ethereum and Solana, as well as permissioned or private networks like JPMorgan’s Kinexys and the Canton Network. [11] [12] CCIP also connects blockchain systems to traditional financial infrastructure, including SWIFT, the global messaging network used by thousands of banks and financial institutions worldwide. [13] This makes CCIP far more than just a web3 blockchain interoperability solution.

CCIP operates through a decentralized network of independent node operators who must reach consensus on the validity of every cross-chain request before it’s executed. This consensus-based approach, combined with cryptographic safeguards, makes CCIP one of the most secure cross-chain solutions currently available. Unlike alternative interoperability protocols such as LayerZero, which suffered a major security incident in April 2026 resulting in approximately $292 million in losses through the Kelp DAO rsETH bridge exploit, or Wormhole, which was exploited for $325 million in February 2022, Chainlink CCIP has maintained a clean security record with no major hacks since its launch. [14] [15] [16]

This strong security track record has been the main reason for many high-profile migrations to CCIP. More than $3 billion in TVL has recently migrated to CCIP. [17] Major projects choosing CCIP specifically for its proven security include Kelp DAO, Solv Protocol (tokenized Bitcoin with over $700 million in assets), Re (on-chain reinsurance protocol), Tydro (leading lending protocol on Kraken’s Ink chain), Kraken (for kBTC and future wrapped assets), and Lido (for wstETH cross-chain transfers), with Lido describing cross-chain infrastructure as “one of the most important security decisions” in its choice to use Chainlink CCIP for wstETH. [18] Coinbase also selected CCIP as its exclusive bridge infrastructure for all wrapped assets. [19]

Real-world use: JPMorgan’s Kinexys and Ondo Finance used CCIP in their 2025 atomic Delivery-versus-Payment (DvP) pilot, enabling simultaneous settlement of tokenized Treasuries and USD payments across public and private chains. [20] State Street’s Galaxy SWEEP fund uses CCIP for secure cross-chain interoperability and stablecoin-based liquidity management. [21] Many tokenized asset platforms also rely on CCIP to move assets between public and private networks, making it a core infrastructure component for institutional tokenization projects [16].

4) Proof of Reserve

Proof of Reserve is one of Chainlink’s most important services for institutional adoption. It allows issuers of stablecoins, tokenized funds, or other real-world assets to publish cryptographically verified attestations on-chain, proving that their reserves fully back the issued tokens at any given time. Independent node operators fetch data directly from custodians or off-chain sources, verify it, and publish a signed report to the blockchain. This provides transparency and auditability without exposing sensitive internal information. [22]

Real-world use: Proof of Reserve has become a de-facto standard for institutional-grade tokenized assets seeking regulatory comfort and investor trust. World Liberty Financial’s USD1 stablecoin, which has a market cap over $4.4 billion and is associated with the Trump family, uses Chainlink Proof of Reserve for real-time, on-chain verification of its reserves. [23] Backed Finance integrates Chainlink Proof of Reserve for its bTokens, which are tokenized stocks and real-world assets. [24] Coinbase also uses Chainlink Proof of Reserve for cbBTC, which has over $6 billion in value, to verify the reserves backing its wrapped Bitcoin. [25]

5) NAVLink and SmartData

NAVLink and SmartData deliver verified Net Asset Value (NAV), Assets Under Management (AUM), and fund performance data directly on-chain for tokenized funds and ETFs. These services are specifically designed for institutional use cases where funds need to publish accurate, auditable valuations in real time or on a daily basis. [26]

Real-world use: NAVLink and SmartData have become essential tools for institutional tokenized funds that require transparent and verifiable valuations. Major traditional ETF issuer VanEck uses Chainlink NAVLink for its VBILL tokenized treasury fund to provide accurate, on-chain NAV data. [27] Amundi, Europe’s largest asset manager with over 2.3 trillion euros in assets under management, uses Chainlink NAVLink for its SAFO tokenized money market fund launched with Spiko. [28] Another major traditional ETF issuer WisdomTree also leverages NAVLink and SmartData for its CRDT tokenized private credit and alternative income fund to deliver real-time, verifiable fund valuations on-chain. [29] In an early production use case, Sygnum tokenized $50 million out of Fidelity International’s $6.9 billion Institutional Liquidity Fund and used Chainlink NAVLink to publish the official NAV on-chain for the tokenized portion. [30]

6) Automation

Chainlink Automation enables smart contracts to trigger functions automatically based on time, price thresholds, or other conditions, without requiring a human or centralized keeper to initiate the transaction. This removes a major friction point in DeFi and tokenized finance by allowing truly autonomous execution. [31]

Real-world use: Many DeFi protocols rely on Chainlink Automation for tasks such as auto-compounding yields, executing limit orders, and performing routine maintenance. [32] Leading examples include Aave for automated collateral management and yield optimization [32] and MakerDAO for various protocol maintenance tasks such as keeper operations and liquidation automation. [33]

7) Functions

Chainlink Functions is a decentralized, serverless compute platform that allows smart contracts to call any off-chain API and run custom JavaScript logic in a secure, verified environment. It gives developers enormous flexibility to bring almost any external computation or data source on-chain, without the high gas costs or technical limitations of trying to do everything directly on the blockchain. [34]

Real-world use: Coinbase’s Project Diamond, its institutional-grade tokenized asset platform, uses Chainlink Functions to enrich tokenized assets with high-quality, real-world data across any chain. [35]

8) VRF (Verifiable Random Function)

Chainlink VRF provides provably fair, cryptographically secure randomness that smart contracts can use for games, NFT minting, lotteries, and any application that requires unpredictable outcomes. [36]

Real-world use: Base, Coinbase’s Layer 2 blockchain, has integrated Chainlink VRF. [37] This allows developers building on Base to access secure, tamper-proof randomness directly in their smart contracts for applications such as prize draws, randomized rewards, gaming features, and fair protocol mechanics.

9) Smart Value Recapture (SVR)

Smart Value Recapture, also referred to as SVR Feeds, is a premium enhancement built directly on top of Chainlink Data Feeds. It enables DeFi protocols to recapture Oracle Extractable Value (OEV), a clean, non-toxic form of Maximal Extractable Value (MEV) that typically arises during liquidations and other price-sensitive events. Instead of broadcasting price updates publicly (where external searchers can extract the value), SVR routes them through a private transmission flow combined with an on-chain auction. Searchers bid for the right to execute the liquidation, and the winning bid is automatically split between the DeFi protocol (to boost revenue or improve user terms) and the Chainlink network. Protocols adopt SVR with minimal changes, they simply point to an SVR-enabled feed address instead of a standard one. [38] [39]

Real-world use: Aave was the first major protocol to integrate SVR on Ethereum mainnet in March 2025 and remains its flagship adopter. By early 2026, SVR had helped Aave recapture more than $16.7 million in non-toxic liquidation MEV on Ethereum across thousands of events while processing hundreds of millions in liquidation volume. [40] The solution has since expanded to additional chains and markets, turning previously leaked value into a growing, sustainable revenue stream for both leading DeFi platforms and the Chainlink ecosystem.

How the Services Work Together via CRE

The real power of Chainlink lies in how all of its services are designed to interoperate as a unified infrastructure layer. The Chainlink Runtime Environment (CRE) is the orchestration engine that makes this possible. It lets developers combine Data Feeds, SVR, CCIP, Proof of Reserve, NAVLink, Automation, Functions, and other capabilities into complex, end-to-end workflows that run securely across public and permissioned blockchains. [41][42]

For example, a tokenized fund workflow could use Chainlink services such as NAV data feeds, CCIP for cross-chain transfers, Proof of Reserve for transparency, and Automation for operational tasks, with these components orchestrated through CRE workflows across public and permissioned blockchain environments. This unified approach is already being used at scale: Swift, Euroclear, and 22 leading financial market participants rely on CRE to streamline corporate actions processing across global markets. [43] [44]

IV. Token Economics

Chainlink’s token economics stand out in the digital assets world because they are built for real revenue capture rather than speculative token sales or endless inflation. The LINK token is not just a governance token or a speculative asset; it functions as the economic glue that aligns incentives across users, node operators, stakers, and the broader network. It serves three core purposes: it’s used (or converted into) for paying for oracle services, it’s staked as collateral to back performance guarantees, and, through the Chainlink Reserve, it directly absorbs value from both decentralized usage and institutional adoption. This design creates a clear flywheel: more usage generates more revenue, which flows back into LINK demand and network security.

Chainlink Payment Abstraction

The mechanism that makes this flywheel possible is Chainlink Payment Abstraction, launched in March 2025 and significantly expanded in August 2025. This August expansion was especially important because it officially extended Payment Abstraction to support off-chain payments, including traditional fiat currencies (such as USD) processed through enterprise agreements. In practice, it removes one of the biggest barriers to adoption: the need for users or enterprises to hold and pay in LINK upfront. Developers, DeFi protocols, or institutional clients can now settle fees in whatever asset they already hold, ETH for gas, USDC or other stablecoins, or even off-chain fiat equivalents. Payment Abstraction then handles the rest automatically. Using Chainlink’s own services (Automation to trigger the process, Price Feeds for accurate pricing, and CCIP to move value across chains), the system consolidates payments, swaps them into LINK on decentralized exchanges such as Uniswap, and routes the LINK to the appropriate recipients. The result is a seamless user experience while ensuring that real economic activity ultimately strengthens the LINK token and the network. [45] [46]

The Chainlink Reserve

At the heart of Chainlink’s evolving economics sits the Chainlink Reserve, an on-chain smart contract launched on August 7, 2025 that turns real network revenue into long-term LINK demand and network sustainability. [46] In simple terms, it acts as a strategic treasury that strengthens the entire oracle network while still making sure the people who actually run the nodes get paid for their work.

To understand how it works, it helps to separate two types of revenue. On-chain payments come from DeFi protocols, dApps, or crypto-native users who pay directly on the blockchain in assets such as USDC or ETH. [45] For regular high-frequency services like standard Data Feeds, most CCIP messages, Automation, Functions, and VRF, 100% of the Chainlink Network’s share still goes directly to node operators. If those on-chain payments are made in non-LINK assets, Payment Abstraction converts them to LINK and deposits the tokens into the Reserve contract first. The full amount is then earmarked for the node operators who performed the service, and they can withdraw it exactly as they would with any other fee.[45] The only clear exception is Smart Value Recapture when the feed is secured by staking: in that case, 50% of the Chainlink Network portion now flows into the Reserve instead of going entirely to operators. [46]

Off-chain payments work differently. These are the enterprise and institutional deals where banks, asset managers, or traditional companies pay in fiat currencies or preferred currencies through invoices or enterprise agreements. Importantly, this revenue is generated as commercial platform access or licensing fees paid to Chainlink Labs, rather than direct per-job compensation to individual node operators. Historically, such income has been recorded on Chainlink Labs’ balance sheet as SaaS-like platform revenue, making it structurally closer to a subscription model than a gig-economy system paying discrete tasks to node operators. Node operators continue to run the existing decentralized infrastructure 24/7 and are compensated separately through regular oracle rewards and on-chain user fees. Since the launch of the Chainlink Reserve, off-chain enterprise revenue is first converted into LINK via Payment Abstraction and then deposited into the Chainlink Reserve contract.

These conversions are batched and executed programmatically rather than in real-time or irregularly, which is why we see fairly regular weekly inflows showing up directly in the LINK Reserve on-chain. [45] [46] The batching happens on a practical weekly schedule for efficiency: lower gas costs, reduced slippage/market impact from one big swap, and smoother execution overall. At the current level of adoption and revenue, that batch size lands in a similar range each week. The amounts have grown slowly over time (e.g., from ~80–90k LINK per week late last year to 120k+ now), which tracks with rising adoption. This pattern lines up closely with Chainlink’s overall network revenue, which has also stayed relatively stable but shown gradual growth since the Reserve launched in August 2025. According to Token Terminal, an institutional-grade on-chain analytics platform, monthly network fees rose from about $4.3 million in August 2025 to roughly $5.8 million by April 2026, and the vast majority of that revenue comes from enterprise and institutional deals. [55] As a result, the steady but slowly increasing weekly inflows we see on-chain make perfect sense and track the same upward trend. As revenue scales (more enterprise deals, more on-chain volume), the weekly purchases should get bigger too. [49]

That said, although that’s what Chainlink says officially, it’s important to note that there is no independent third-party audit or external confirmation that every dollar of Chainlink Labs’ enterprise/off-chain revenue is converted into the LINK Reserve via Payment Abstraction. It ultimately relies on Chainlink Labs’ own statements and internal processes. The mechanism exists and is used (inflows are happening and growing), but there is no independent proof that it captures literally all enterprise revenue with zero exceptions. Even so, Chainlink Reserve is designed as a strategic, long-term treasury that supports the network’s growth and sustainability, with no withdrawals expected for multiple years. [46]

Since launch the Reserve has grown steadily and transparently. It started with just over $1 million worth of LINK in the early launch phase. By mid-2026 it holds approximately 3.66 million LINK, valued at roughly $34 million, with an average cost basis around $12.58. You can watch every inflow live on the public dashboard at reserve.chain.link. [47] As institutional tokenization continues to scale, the Reserve is positioned to become one of the clearest mechanisms tying Chainlink’s real-world usage directly to long-term token value accrual. [48]

This design is what allows the Reserve to grow steadily. Every new dollar of qualifying revenue, especially from high-value institutional adoption and the 50% SVR allocation, adds LINK to the contract. The strategic slice remains protected and accumulates over time. The more revenue the network generates, the faster the Reserve grows. It’s a direct, usage-driven mechanism that ties real-world adoption to long-term network security and LINK value accrual without relying on token burns or inflation.

Staking economic model

The network’s staking model adds a second layer of cryptoeconomic security and gives LINK holders a direct way to participate in the network’s growth. Launched in its current form as Staking v0.2, the program lets both community members and professional node operators commit LINK as collateral to back high-priority oracle services. The total staking pool is capped at 45 million LINK, roughly 8% of the current circulating supply, split between a community pool of 40.875 million LINK and a smaller allocation reserved for vetted node operators. [49] [50]

Community stakers face no slashing risk and simply lock LINK to help secure the network. They earn a variable reward rate that starts with a base floor of 4.5% per year. Because 4% of those community rewards are automatically delegated to node operators as a service fee, the effective base rate for community stakers is approximately 4.32% when the pool is full. The actual APY fluctuates in real time depending on how full the pool is: when there is unfilled capacity, the same fixed amount of rewards is spread across fewer stakers, pushing the rate higher. This dynamic design incentivizes the pool to stay full while still delivering attractive yields to participants. [49] [51]

Node operator stakers, on the other hand, commit larger minimum amounts (typically 1,000 to 75,000 LINK per operator) and take on slashing risk for the specific services they secure. In return they receive their own base rewards plus the delegation rewards from community stakers, which can push their effective yields noticeably higher. [50]

Right now the roughly 4.32% APY paid to community stakers is still largely funded by protocol emissions, new LINK tokens released from the remaining uncirculated supply (the 273 million LINK that have not yet entered circulation). Over time, however, Chainlink is deliberately shifting the reward structure away from these emissions and toward real user fees generated by the network. [50] As revenue from Payment Abstraction, the 50% SVR redirection, enterprise deals, CCIP, and other services continues to grow, an increasing share of that revenue will flow into the staking reward pool. This gradual transition means APY will become more directly tied to actual network usage rather than inflation.

Node operator economics

Node operators are the backbone of the Chainlink network, the independent entities that run the decentralized oracle nodes, fetch and validate off-chain data, and deliver it on-chain with cryptographic proofs. Their economics are deliberately attractive because they bear real operational costs: reliable servers, premium data subscriptions, gas fees, 24/7 monitoring, and redundant infrastructure to maintain uptime. In return they earn the majority of direct service fees from the products they support. [52]

For regular high-frequency services such as standard Data Feeds, most CCIP messages, Automation, Functions, and VRF, operators receive 100% of the Chainlink Network’s share of the fees. High-value services like SVR add an extra revenue stream, though a portion of staking-secured SVR fees is redirected to the Reserve. Operators who also stake receive additional rewards through delegation from community stakers and can earn higher yields on services they help secure. Selection for premium feeds is reputation-based: only operators with proven uptime, security posture, and performance are whitelisted. [52] [46]

As Chainlink adoption continues to rise, the economics become even more compelling. Higher network usage drives up fee revenue per operator, which in turn creates a very attractive ROI for running a node. This growing revenue naturally incentivizes new professional operators to join the network. To participate in the highest-paying production services, these new operators must first meet Chainlink Labs’ strict requirements, demonstrating reliable infrastructure, strong security practices, and a proven track record of uptime and performance. Once approved, they typically buy LINK on the open market and stake up to 75,000 LINK each into the dedicated Node Operator Staker Allotment. This stake serves as skin in the game, signaling credibility and alignment with the network’s security. [52] [46]

Historically, the number of whitelisted node operators has increased over time as the network has scaled, growing from just a handful in the early days to dozens of professional teams today. Chainlink Labs has also raised the overall staking cap before (when upgrading from v0.1 to v0.2) and the design allows for future increases as adoption grows. [49] [50] The result is a powerful flywheel: more adoption leads to higher revenue per node, which attracts more operators, who in turn buy and lock up additional LINK to secure their position. This creates both buying pressure and long-term holding pressure on the token, strengthening the overall economics of the LINK token.

The combination of fee income plus staking rewards has historically allowed top operators to generate substantial revenue, in some cases hundreds of millions cumulatively since mainnet launch [53], while the ongoing shift toward real usage fees (instead of emissions) makes their business model increasingly sustainable. Node operators run a professional infrastructure business that is directly compensated by network activity, and the growing usage naturally draws in more capital and more operators. [52] [46]

V. Revenue Analysis and Growth Drivers

This section examines the current state of Chainlink’s revenue, its key growth drivers, and the practical interplay between revenue generation and token supply/demand dynamics. While the launch of the Chainlink Reserve and the expansion of Payment Abstraction in August was an important inflection point, the network’s economics are still in a relatively early phase. Revenues have grown meaningfully, but they remain modest relative to the ~70 million LINK released annually through scheduled unlocks. Achieving genuine scarcity for LINK and long-term value accrual will require sustained revenue growth at a scale that consistently outpaces selling pressure, with a rising share of that revenue flowing into the Chainlink Reserve and staking pools. This outcome is not automatic. It depends on continued institutional adoption, higher CCIP volumes, broader enterprise integration, and the ability of tokenized assets to move from pilots to mainstream production use.

Breakdown of Current Revenue Sources

Data Feeds remain the single largest contributor to total network revenue and have historically accounted for the majority of fees paid to node operators. [54] Monthly revenues have now reached approximately $4.5–5.8 million [55] and have entered a consolidation phase. This is not surprising.

Large institutional integrations and production rollouts simply take time. They involve lengthy legal agreements, compliance reviews, rigorous testing, and gradual scaling before moving from pilot programs to meaningful revenue. Regulatory clarity is also still developing; the Clarity Act has not yet become law, and the CFTC and SEC are expected to issue detailed rulebooks within roughly 12 months once major legislation passes.[56]

A common criticism heard in the market is that, despite the impressive list of high-profile partnerships with DTCC, SWIFT, Fidelity, and others, the actual on-chain accumulation in the Chainlink Reserve and overall network revenue have grown only modestly and steadily rather than seeing sharp jumps. This observation is understandable. A partnership announcement is the beginning of a process, not the end. Just as a restaurant owner signing an agreement with a top table-booking platform doesn’t mean the restaurant will suddenly be fully booked every night, institutional tokenization partnerships don’t automatically translate into large-scale revenue overnight.

The key context is that the tokenized real-world asset market itself remains very early. At roughly $33 billion globally as of mid-2026, [63] it still represents only a tiny fraction of the hundreds of trillions in traditional financial markets. If tokenized asset volumes from major institutions that have partnered with Chainlink had already reached the trillions while network fees and weekly Reserve inflows remained negligible, then the criticism that accumulation is “too slow relative to the hype” would carry real weight. But that is not the situation today. The current pace of revenue and Reserve inflows is consistent with the early stage of a multi-year transition.

Even so, the underlying growth signals are strong. CCIP has become the standout growth driver. According to Chainlink’s official Q1 2026 data, transfer volume on CCIP grew 78% quarter-over-quarter and 319% year-over-year, while the number of tokens active on CCIP rose more than 165% year-over-year and CCIP fee revenue itself increased 213% quarter-over-quarter. [48] In practical terms, this means institutions and protocols are moving dramatically more value across blockchains using Chainlink, from tokenized Treasuries and equities to stablecoin liquidity and cross-chain governance, generating significantly higher fees in the process. This growth reflects real institutional adoption rather than speculative DeFi activity.

Another strong signal of accelerating institutional interest is the adoption of the Chainlink Runtime Environment (CRE). Sign-ups for CRE grew 50% month-over-month in Q1 2026, while total workflow executions on CRE increased 253%. [48] CRE is the orchestration layer that allows institutions to build complex, end-to-end on-chain workflows combining multiple Chainlink services with compliance, privacy, and legacy system connectivity. The sharp rise in sign-ups shows more teams are starting to explore CRE, while the 253% jump in actual workflow executions indicates that many of these teams are moving beyond testing and running real production processes. In practice, this points to growing use in areas such as tokenized fund management, atomic delivery-versus-payment settlement, and automated corporate actions, precisely the high-value institutional use cases Chainlink has been targeting.

Off-chain enterprise revenue, payments from banks, asset managers, and tokenized-fund issuers, has also accelerated sharply and now represents a fast-growing share of inflows into the Chainlink Reserve. [46] [54] Stablecoins and non-stablecoin RWAs both play important roles. Stablecoin-related activity (Proof of Reserve attestations, cross-chain transfers, and liquidity management) has been a steady contributor, while non-stablecoin RWAs, especially tokenized Treasuries, equities, and private credit funds, are driving the newest wave of demand. Institutional platforms such as VanEck’s VBILL, Amundi’s SAFO, WisdomTree’s CRDT, and Backed’s xStocks all rely on Chainlink for NAVLink, Proof of Reserve, Data Streams, and CCIP. The result is a broadening revenue base that is less dependent on pure DeFi cycles and more tied to real-world asset tokenization.

The Institutional Adoption Wave and Future Revenue Potential

The current monthly network fees represents a meaningful progress, but they are still modest in the context of the multi-trillion-dollar tokenized asset opportunity. Given the accelerating trajectory of Chainlink’s institutional partnerships and the global growth in tokenization, the opportunity for substantial revenue scaling appears highly promising.

Major institutions and platforms are increasingly designating Chainlink as their official oracle infrastructure, including DTCC, SWIFT, Euroclear, Kraken, Robinhood, FTSE Russell, Amundi (Europe’s largest asset manager), Fidelity International, UBS, and Mastercard. Ondo Finance has named Chainlink the official oracle provider for all its tokenized stocks and ETFs, and Backed xStocks (live on Kraken and Bybit) uses Chainlink Data Streams and Proof of Reserve for all tokenized U.S. equities and ETFs. Tokenized equities and ETFs are growing particularly fast, and Bloomberg has reported that the Trump administration is poised to roll out plans for trading digital versions of securities that could reshape the U.S. stock market. [57] [58] Credible forecasts from BCG, McKinsey, Citi, and Standard Chartered project the tokenized asset market to reach trillions of dollars by 2030–2033. [58] [59] [60] As more sovereign bonds, Treasuries, equities, and alternative assets move on-chain, Chainlink’s enterprise revenue is expected to scale significantly.

While the current network revenues are still in a consolidation phase, the combination of surging CCIP volume, accelerating CRE adoption and expanding institutional partnerships positions Chainlink for potentially significant revenue growth in the years ahead. The network’s economics are shifting from being dominated by mature on-chain Data Feeds to a more diversified base that includes high-value enterprise and tokenized-asset workflows. This transition is exactly what will determine whether the token supply dynamics move from inflationary to neutral or even deflationary over time.

Token Unlocks, Dilution, and the Long-Term Outlook

At present, the Chainlink network remains inflationary. With roughly 727 million LINK in circulation as of May 2026 and approximately 273 million still scheduled to enter through quarterly unlocks (at a rate of ~7% of total supply, or roughly 70 million LINK per year), the net supply continues to expand. [61] A significant majority of these unlocked tokens are transferred to Binance shortly after each quarterly release [106]. This structural reality has made it difficult for the token to build sustained value accrual, even as network usage and revenue have grown. Many market participants have noted that LINK has felt “stuck” despite meaningful progress on the adoption front. This is not a failure of execution so much as a reflection of where we are in the cycle: this is still a very early phase.

Tokenization of real-world assets, enterprise blockchain adoption, and the deeper integration of traditional finance into on-chain infrastructure remain a tiny fraction of their ultimate potential. The vast majority of global financial activity, securities settlement, fund administration, and cross-border payments still occurs through legacy systems. What we are seeing today with announcements from the likes of Ondo, Backed, VanEck, Amundi, and others represents the very beginning of a multi-year transition. In this context, it’s unsurprising that protocol revenue, while growing, has not yet reached a scale capable of fully offsetting ongoing token issuance.

That said, Chainlink has taken deliberate and strategically important steps to position itself for when that transition accelerates. The launch of the Chainlink Reserve combined with Payment Abstraction was not merely a technical upgrade, but materially improved the alignment between enterprise adoption and long-term tokenomics by ensuring that a growing share of revenue supports the network’s economic sustainability.

It’s also notable that major institutions have chosen to work with Chainlink rather than alternatives such as Pyth Network or Redstone, or building proprietary solutions. Organizations including DTCC, SWIFT, Euroclear, Amundi, Fidelity International, and UBS have integrated Chainlink for production use cases involving NAV data, Proof of Reserve, and cross-chain messaging. These decisions were not inevitable. They reflect a preference for Chainlink’s combination of decentralization, security track record, and institutional tooling. Over time, this creates a meaningful economic moat as more critical infrastructure is built on top of the network.

This positioning matters for tokenomics. In Q1 2026, the Reserve added over 1.47 million LINK, with an annual accumulation run-rate of roughly 6 million LINK [40]. This buy-and-lock mechanism, funded by both on-chain fees and off-chain enterprise revenue, is already generating counter-pressure against new token issuance. As institutional volume scales, these inflows are expected to increase. Today, monthly revenue of around $5 million remains modest relative to the roughly 70 million LINK issued annually. Inflation is still the dominant force. However, the structural setup has improved. Once the remaining tokens enter circulation toward the end of the decade [62] and revenue continues to grow, the combination of higher Reserve inflows, staking, and increased protocol revenue creates a plausible path toward deflationary dynamics.

A common criticism is that value accrual to the token can still feel relatively indirect and modest at this stage. A meaningful share of revenue continues to support node operators and network security first, while the Chainlink Reserve’s accumulation, although growing steadily, has delivered only gradual rather than more immediate results. Compared to certain newer protocols that use more aggressive or direct mechanisms, Chainlink’s token economics can appear slower and less forceful in their effect. This design was intentional. Chainlink prioritized building a robust, decentralized network and long-term sustainability over faster or more direct impact on market capitalisation. Whether this model ultimately creates stronger and more durable economic alignment will depend on whether network revenue scales significantly faster than token issuance in the years ahead. Given that tokenization remains in its very early stages globally, the current pace is consistent with a multi-year transition rather than a shortcoming of the mechanism itself.

VI. Tokenization Market Opportunity

The tokenization of real-world assets represents one of the most significant structural shifts underway in global finance. While still early, the movement of traditional financial instruments onto blockchain rails is gaining meaningful traction, driven by improvements in efficiency, transparency, and accessibility. Understanding the current scale, credible growth projections, and the types of assets likely to dominate the next phase is essential to assessing both the opportunity and the infrastructure required to support it.

Current Size of Tokenized Real World Assets

Source: Bitwise

As of May 2026, the tokenized real-world asset (RWA) market has moved well beyond the experimental stage. According to RWA.xyz, the total distributed asset value of tokenized RWAs stood at approximately $33 billion as of May 21, 2026 [63]. This represents meaningful progress from earlier in the year, with the market growing by roughly 30% during Q1 2026 alone.

Growth has been highly concentrated in a few categories, most notably tokenized U.S. Treasuries and tokenized equities. While the overall RWA market remains small relative to traditional finance, the speed of expansion in certain segments has been notable.

(1) Tokenized U.S. Treasuries

Tokenized U.S. Treasuries remain by far the largest part of the RWA market. This category is currently valued at around $15.3 billion, up from $9 billion at the start of the year and roughly $6.6 billion twelve months ago [63]. That represents approximately 70% growth year-to-date and more than 130% growth over the past twelve months.

The broader U.S. Treasury market itself is enormous. Outstanding marketable Treasury debt stands at roughly $30.7 trillion as of April 2026, making it one of the largest and most liquid asset classes in the world [64]. When measured against the tokenized portion, the on-chain segment is still tiny, less than 0.05% of the total market. In practical terms, this shows how early the tokenization wave still is, even though the absolute numbers have grown rapidly in the past year.

Tokenizing Treasuries matters because U.S. government debt is the world’s primary collateral asset. It sits at the heart of global finance, used by banks, hedge funds, central banks, and corporations for liquidity, risk management, and settlement. Bringing even a fraction of this market on-chain could deliver meaningful advantages: near-instant settlement, 24/7 availability, programmable collateral rules, and reduced operational friction. A credible analysis from McKinsey highlights that tokenization of fixed-income assets such as Treasuries can improve operational efficiencies by at least 40% through automation, better data clarity, and streamlined processes across the asset life cycle [65]. These gains are not theoretical and they address real pain points in today’s multi-day settlement cycles and fragmented collateral management.

The current momentum in tokenized Treasuries is coming from two main groups of players: major custodians and leading asset managers.

Custodians and Market Infrastructure

Traditional custodians already dominate the custody and settlement of U.S. Treasuries in the legacy world. BNY Mellon, State Street, JPMorgan, DTCC, and Euroclear together handle trillions in Treasury assets and serve as the backbone of global settlement and safekeeping.

BNY Mellon has moved into production use cases. In 2025 it was appointed investment manager and primary custodian for OpenEden’s $TBILL tokenized Treasury fund, the first such product to receive an investment-grade rating from Moody’s while backed by a global custodian [66]. This arrangement gives OpenEden institutional-grade custody while keeping the fund on-chain.

State Street has launched its Digital Assets Platform, which includes wallet management, custody, and cash capabilities specifically designed to support tokenized products, including debt and money-market funds [67]. The bank is also integrating with other blockchain settlement systems to enable digital wallets that represent institutional holdings of bonds and Treasuries.

Euroclear, one of Europe’s largest central securities depositories, is actively developing and operating distributed ledger technology infrastructure through its Digital Financial Market Infrastructure platform. The platform enables the issuance and settlement of digitally native securities, mainly bonds, while maintaining full integration with Euroclear’s existing traditional settlement systems [68]. It participates in multi-institution pilots focused on tokenized bonds, funds, and collateral, with an emphasis on corporate actions automation and interoperability [69].

JPMorgan has been one of the most aggressive. Through its Kinexys platform it has executed live pilots involving tokenized U.S. Treasuries, including cross-chain delivery-versus-payment (DvP) transactions. In one notable example, JPMorgan handled the cash leg while tokenized Treasuries were settled in real time on a public blockchain [70]. These tests show that major banks can connect permissioned banking rails with public-chain assets in near-real time, which could eventually reduce settlement risk and unlock 24/7 liquidity.

DTCC, the central securities depository for the U.S. market, is advancing its own tokenized infrastructure. Its flagship Project Ion is building a parallel settlement platform on distributed ledger technology that aims for faster, near-real-time settlement of tokenized collateral, including Treasuries and repo [72] [72]. DTCC is also developing standards for interoperability between blockchains and legacy systems [73].

Asset Managers and Tokenized Money Market Funds

On the issuance side, several large asset managers have brought regulated Treasury-backed products on-chain. BlackRock, the world’s largest asset manager, launched its BUIDL fund in March 2024 with an initial seed of around $100 million. By March 2025 the fund had crossed $1 billion in assets under management, which represented roughly 900% growth in its first twelve months. As of May 2026 it has surpassed $2.5 billion, an additional 150% increase over the following 14 months and more than 2,400% growth overall since launch [74]. The fund offers qualified U.S. investors on-chain exposure to short-term Treasuries with daily liquidity and programmable features.

Circle’s USYC, aimed primarily at non-U.S. persons, has grown to approximately $2.9–3 billion in assets. The fund (originally launched by Hashnote and later acquired and expanded by Circle) stood at roughly $635 million in October 2025. By March 2026 it had crossed $2 billion, and it reached nearly $3 billion by May 2026, representing roughly 370% growth in just seven months and more than fourfold growth over the past year [75]. International investors have been drawn to its regulated structure and the ability to redeem directly into USDC on a near-instant basis.

Franklin Templeton’s BENJI fund was one of the earliest U.S.-registered tokenized money-market products when it launched in 2021. It has steadily scaled across multiple blockchains and now forms part of a suite that exceeds $1.5–2 billion in assets. From a base of around $690 million in mid-2025, the BENJI suite has grown by more than 180% in the past twelve months, with investor numbers increasing over 140% between April 2024 and March 2026 [76]. The fund offers peer-to-peer transfers and direct USDC conversion, making it one of the more mature and accessible options for both institutional and retail participants.

UBS has also entered the space with its UBS USD Money Market Investment Fund Token (uMINT), launched in November 2024. This provides another institutional-grade option for tokenized Treasury exposure [77]. More recently, Fidelity International launched its first tokenized U.S. dollar liquidity product in May 2026. The fund is powered by Sygnum’s Desygnate tokenization platform, with J.P. Morgan providing fund administration and custody services and Apex Group acting as transfer agent. It offers 24/7 subscriptions and redemptions, stablecoin integration, and has received an AAA-mf assessment from Moody’s for its strong ability to meet objectives of capital preservation and high liquidity [78]. This latest addition from one of the world’s largest traditional asset managers further signals the broadening institutional interest in regulated, always-on Treasury liquidity solutions.

Broader Initiatives Showing Momentum

Several recent developments point to continued institutional commitment. The Bank of England, together with the FCA, has proposed extending settlement infrastructure toward near-24/7 operations to prepare UK wholesale markets for tokenized finance [79]. In Europe, regulated pilots for tokenized government bonds are moving into early production, with the ECB developing supporting infrastructure under a 2026–2028 roadmap [80]. Japan is testing tokenized Japanese Government Bonds (JGBs) as digital collateral on the Canton Network, involving institutions such as JSCC, Mizuho, and Nomura, while the Bank of Japan continues experiments with blockchain-based reserves and interbank settlement [81].

Chainlink’s Supporting Role

Chainlink has played a supporting role across many of these efforts. Ondo has built one of the more extensive integrations, using both price oracles and CCIP to power parts of its tokenized Treasury offerings [82]. Superstate has incorporated Chainlink oracles to publish NAV data on-chain [83]. Fidelity and Sygnum partnered with Chainlink to bring NAV data onchain to enable the tokenization of Fidelity’s USD Digital Liquidity Fund (FILQ) [84]

Beyond individual funds, Chainlink is involved in broader institutional pilots and collaborations. SBI Digital Markets (part of Japan’s SBI Group) has selected Chainlink CCIP as its exclusive cross-chain interoperability solution for tokenized securities and funds [85]. DTCC is integrating Chainlink data standards and the Chainlink Runtime Environment into its Collateral AppChain for 24/7 tokenized collateral management [43]. Euroclear participates in multi-institution initiatives with Chainlink focused on corporate actions automation and asset servicing standardization [69]. JPMorgan’s Kinexys platform has used Chainlink in cross-chain DvP experiments involving tokenized Treasuries [86]. BNY Mellon and State Street appear in the wider Chainlink institutional ecosystem through custody and tokenization pilots where issuers rely on Chainlink services [87].

Taken together, the combination of major custodians, asset managers, and infrastructure providers moving into production or advanced pilots suggests tokenized Treasuries are transitioning from experimentation to a more established part of institutional finance.

(2) Tokenized Credit

Tokenized credit has grown more aggressively than many other segments. The category is now worth approximately $5.2 billion, up from around $1.29 billion one year ago [63]. This represents roughly 300% growth (or more than fourfold expansion) over the past twelve months. Much of this growth has come from platforms offering on-chain exposure to private credit and other forms of institutional lending, where transparency, programmability, and faster settlement provide clear advantages over traditional private-market structures.

Maple Finance has been one of the more established names in this area, along with products like SyrupUSDC. These platforms have attracted capital from both DeFi users and more traditional investors looking for yield outside of public markets. Chainlink supports parts of this ecosystem by providing oracle data. Maple, for example, has integrated Chainlink oracles to improve pricing transparency and data reliability for its credit products [88].

(3) Tokenized Stocks and Equities

Source: Token Terminal

Tokenized equities have been one of the faster-growing parts of the RWA market in percentage terms. The category has reached roughly $1.7 billion, up from $682 million at the beginning of the year and just $320 million one year earlier [92]. That represents more than 149% growth year-to-date and approximately 431% growth (or more than 5x expansion) over the past twelve months.

Ondo Global Markets has led the way, crossing $1 billion in TVL in May 2026, less than eight months after launch [89]. Other platforms, including xStocks and those built with Securitize, have also contributed to higher trading volumes and greater visibility for tokenized stocks.

Chainlink’s infrastructure is being used across several of these platforms. Ondo has one of the deeper integrations, relying on Chainlink for price data, cross-chain transfers, and reserve verification [82]. Other tokenized equity products, like xStocks, have also incorporated Chainlink oracles to support accurate pricing [10].

(4) Tokenized Commodities

Tokenized commodities currently sit at around $7 billion, up significantly from $2.2 billion one year ago [63]. That represents roughly 218% growth (or more than triple the size) over the past twelve months. Gold continues to dominate this category, with most of the value concentrated in a small number of established products.

Paxos Gold (PAXG) remains the largest tokenized commodity by some margin. Interest in this area has been steadier than in some other segments, reflecting ongoing demand for on-chain exposure to traditional stores of value. Chainlink has been involved here for some time through its work with Paxos on Proof of Reserves. This integration allows users to verify on-chain that each PAXG token is backed by physical gold held in custody [90].

(5) Non-U.S. Government Debt

Non-U.S. government debt has also expanded, though it remains smaller than the U.S. Treasuries category. This segment is currently valued at approximately $1.41 billion, up from $434 million one year ago [63]. That represents roughly 225% growth (more than triple the size) over the past twelve months.

Spiko is currently the main player in this space. While growth here has been more gradual, there is clear interest in bringing non-U.S. sovereign and government-backed debt on-chain. Chainlink has partnered with Spiko to provide oracle services and data infrastructure for its tokenized European government debt products [91].

Forecasts for the Size of the Tokenized Asset Market

Source: a16z crypto

Forecasts for the size of the tokenized asset market vary considerably depending on scope and assumptions. Among the most widely referenced projections is the April 2025 report by Boston Consulting Group, which estimates that the broader tokenized asset market (including stablecoins) could grow from roughly $0.6 trillion in 2025 to $18.9 trillion by 2033 in its midpoint scenario. This implies a compound annual growth rate of 53% and reflects expectations of widespread adoption across asset classes, geographies, and use cases [93].

McKinsey & Company has taken a more conservative view. In its June 2024 analysis, it projected that tokenized financial assets could reach around $2 trillion by 2030 in a base case, with an optimistic scenario reaching up to $4 trillion. McKinsey’s estimates deliberately exclude stablecoins and focus on traditional financial instruments such as bonds, funds, loans, and alternative assets [59]. Standard Chartered has offered a more bullish near-term outlook on non-stablecoin RWAs specifically, projecting that this segment alone could reach $2 trillion by 2028. Some of the bank’s updated commentary has pointed toward even higher aggregate tokenized asset figures when including stablecoins [60]. Citi’s June 2026 tokenization report takes a similar view, projecting the market to reach $5.5 trillion by 2030 in its base case. Citi also laid out a more conservative bear case of $2.7 trillion and a bullish scenario of $8.2 trillion [94].

Source: Citi Institute

These forecasts differ in methodology and scope, but they collectively point to the same directional conclusion: even under relatively cautious assumptions, tokenized assets are expected to grow by an order of magnitude over the next seven to eight years. What gives these long-term projections additional credibility is that they are increasingly supported by concrete actions from sovereign governments and major financial market infrastructures. In the past 12–18 months, several nation states have moved beyond pilots and begun integrating tokenization directly into national infrastructure.

Dubai’s Land Department launched a real-estate tokenization initiative in May 2025 in partnership with VARA and Ctrl Alt. The project directly records legal ownership of land title deeds on the XRP Ledger and has set a target of AED 60 billion (approximately $16.3 billion) in tokenized real estate by 2033 [95].

Georgia’s Ministry of Justice signed an agreement with Hedera in late 2025 to explore migrating the country’s entire national real estate registry onto blockchain, potentially enabling nationwide fractional ownership and on-chain property rights [96].

Hong Kong has moved into regular tokenized government bond issuance. In late 2025 the Hong Kong Monetary Authority completed a record HK$10 billion (approximately $1.3 billion) tokenized bond offering through its CMU OmniClear digital asset platform, with plans to scale the infrastructure further [97].

Singapore’s Monetary Authority continues to expand Project Guardian, a multi-year initiative involving more than 40 global banks and institutions focused on tokenized bonds, funds, deposits, and structured products. The program has shifted from experimentation toward building institutional-grade infrastructure [98]. Chainlink serves as a key technology partner in Project Guardian, supplying decentralized oracles and the CCIP to enable secure data delivery, cross-chain transfers, and automated tokenized fund operations in several live institutional pilots [99].

Saudi Arabia has also taken significant steps. Under Vision 2030, droppRWA has secured $12.5 billion in initial mandates to tokenize real estate and other assets, with plans to expand into energy and manufacturing sectors using a sovereign-grade blockchain [100].

Many of these sovereign-level projects are currently focused on static legal records such as property deeds or bond ownership. However, as these initiatives mature and move beyond simple digital registries toward more dynamic, programmable financial applications, the need for reliable external data becomes essential. Real-time market pricing and valuation feeds for oil prices, commodity benchmarks, real estate indices, interest rates, or foreign exchange rates are required if tokenized assets are to be used as collateral in lending markets, to power derivatives, to trigger automatic liquidations, or to support dynamic pricing and yield products. Registry integration alone cannot provide this live market data.

For credibility with global institutions and major international banks, independent verification is equally important. Proof-of-reserve attestations, independent NAV calculations, and fund-level metrics must come from trusted external sources that go beyond any single government system. The same principle applies when governments decide to tokenize or enable trading of assets that sit outside their own domestic registries. Examples include foreign real estate, global equities, international bonds, or commodities traded on exchanges worldwide. These assets also require secure external data inputs to function effectively on-chain and to integrate smoothly into broader global markets.

Saudi Arabia’s expansion plans into energy, manufacturing, and industrial assets make this particularly relevant. These sectors rely heavily on SCADA systems, IoT sensors, production meters, renewable output data, and carbon credit verification, information that does not reside in a central government property registry. Faisal Al Monai, Chairman of droppRWA, has publicly stated that SCADA data will feed data oracles to trigger smart-contract payouts and automated revenue distribution on tokenized energy and manufacturing assets [101]. Without trusted external oracles, real-time, performance-based settlements and automated yield mechanisms simply cannot operate at scale.

Major Traditional Financial Market Infrastructures Advancing Institution-Led Tokenization Projects.

NYSE and Securitize Tokenized Equities Platform

In March 2026, the New York Stock Exchange (part of Intercontinental Exchange) signed a Memorandum of Understanding with Securitize to jointly develop a tokenized securities trading platform. Securitize has been designated the first digital transfer agent eligible to mint blockchain-native stocks and ETFs for issuers on the planned NYSE-affiliated Digital Trading Platform, with the explicit goal of enabling 24/7 trading and on-chain settlement. This is more than exploratory, as Securitize has been granted a formal design-partner role, and the parties are actively collaborating on digital transfer agent standards, market structure, and regulated infrastructure. [102] At this stage the project remains in the development and planning phase and will require regulatory approvals before launch, but the commitment from the NYSE signals serious institutional intent to bridge traditional brokerage rails with blockchain settlement.

Japan’s Push to Tokenize Government Bonds

Similarly, in Japan, one of the world’s largest government bond and repo markets, leading institutions including MUFG, Mizuho, Nomura, Daiwa Securities, JPX, and JSCC (plus over 330 consortium members) have launched a structured initiative via the Progmat-operated Digital Asset Co-Creation Consortium. In May 2026 the consortium formed the “Tokenized Government Bonds & On-Chain Repo Working Group” with the concrete aim of tokenizing Japanese Government Bonds for 24/7 repo trading and stablecoin settlement in a market currently sized around $1.6 trillion. [103] The group has a defined roadmap, including a detailed report in October 2026, parallel proof-of-concept trials, formal project launch within 2026, and targeted commercialization/live operations by the end of 2026. The effort is built on Progmat’s dedicated Avalanche subnet (with over $2 billion in existing tokenized assets already migrating to it) [104] and carries explicit regulatory engagement from Japan’s Financial Services Agency [105].

If these nation-state and major-market initiatives continue to advance beyond registries into fully programmable financial applications (as the NYSE and Japanese repo efforts explicitly aim to do), the demand for reliable external data, such as pricing feeds, collateral valuation, corporate actions, interest rates, and mark-to-market calculations, will become essential. The same principle applies to foreign assets, global equities, commodities, or dynamic repo/lending features. For credibility with global institutions and regulators, independent oracles providing verifiable data and Proof-of-Reserve-style attestations will be required. If these projects mature and Chainlink maintains its established track record of security, reliability, and institutional adoption, the network stands to play a supporting role as a key infrastructure layer.

VII. Institutional Adoption and Real-World Use Cases

While headline partnerships and pilots often sound impressive, the real test for any infrastructure project is whether it solves actual operational pain points for large institutions. In Chainlink’s case, several high-profile collaborations in 2025–2026 have moved beyond announcements into practical testing. Below is a clear-eyed look at the most significant ones, what they actually do, how Chainlink is involved, and why they matter in everyday institutional finance.

(1) Real-Time Settlement Between Cash and Tokenized U.S. Treasuries

In May 2025, JPMorgan, Ondo Finance, and Chainlink successfully completed one of the most practical institutional pilots in tokenized finance to date. They demonstrated a transaction in which an investor could buy tokenized U.S. Treasury fund using actual U.S. dollars held at JPMorgan, with the tokenized asset and the cash payment settling at exactly the same moment [86].

In traditional markets, even large trades usually settle on a T+1 or T+2 basis. This means there is a delay of one or two business days between agreeing on the deal and the actual exchange of money and assets. During that window, both buyer and seller must hold extra collateral and liquidity just in case. Across the entire market, this locks up hundreds of billions of dollars in capital every day that cannot be used for other purposes. Banks and asset managers also incur enormous operational costs for reconciliation, failed-trade management, and back-office staff. [107] Even small fail rates become very expensive at the scale of trillions in daily volume. The pilot eliminated that delay through atomic settlement, where both sides of the trade completed together or were cancelled with no loss to either party.

Chainlink’s Cross-Chain Interoperability Protocol (CCIP) and Runtime Environment (CRE) coordinated the cash leg on JPMorgan’s permissioned network with the tokenized asset on a public blockchain, ensuring everything happened securely and simultaneously [108].

The scale makes this particularly noteworthy. The overall U.S. Treasury market stands at approximately $30.7 trillion, while tokenized U.S. Treasuries have already grown to around $15 billion and continue expanding rapidly. As tokenized Treasuries are forecasted to become a more meaningful part of the broader financial system, the ability to settle instantly and safely between traditional banking rails and blockchain becomes increasingly valuable. It reduces risk, frees up capital that is currently locked for days, and supports more efficient 24/7 operations without forcing institutions to replace their existing systems.

This pilot provides one of the clearest demonstrations yet that tokenized assets can integrate smoothly with traditional finance at institutional scale. If Chainlink’s technology is adopted more widely for these types of delivery-versus-payment workflows by JPMorgan and across the broader banking sector, and if tokenized Treasuries continue scaling toward multi-trillion-dollar volumes, it could generate substantial enterprise network fees for Chainlink over time.

(2) AWS Marketplace Integration

In April 2026, Chainlink made its full suite of services, including Data Feeds, Data Streams, Proof of Reserve, and the Chainlink Runtime Environment, directly available on the AWS Marketplace [109]. This allows any enterprise already using Amazon Web Services to subscribe to Chainlink oracles using the same procurement, billing, and compliance processes they use for other approved cloud tools.

This step carries real practical weight. Many of the exact institutions we have discussed earlier are already heavy AWS users. The New York Stock Exchange relies on AWS for its cloud streaming and market data platforms. In Japan, MUFG has a multi-year strategic preferred cloud agreement with AWS, and the broader Progmat consortium banks run substantial workloads on AWS. As these projects move from simple ownership records toward dynamic features such as collateral management, repo trading, automated settlements, and cross-border liquidity, they will need reliable external data.

By being listed on the AWS Marketplace, Chainlink removes one of the biggest practical barriers for large organizations. According to a Forrester study commissioned by AWS, 72% of respondents reported faster procurement time and a significant reduction in the effort required for vendor onboarding and security reviews [110]. Institutions can now treat Chainlink services like any other approved enterprise software rather than a new blockchain vendor that requires lengthy internal approvals. This dramatically lowers friction and speeds up adoption for the very organizations exploring tokenized assets at scale.

Chainlink is currently the most comprehensive and prominently featured oracle platform on the AWS Marketplace for institutional use cases. While other oracles exist in the broader AWS ecosystem, Chainlink’s full-suite availability through the Marketplace gives it a clear practical advantage with the very organizations that are actively building tokenized infrastructure.

(3) DTCC Tokenization Service

The Depository Trust & Clearing Corporation (DTCC) operates the central infrastructure that clears and settles the vast majority of U.S. securities, holding more than $114 trillion in assets under custody. In December 2025 the SEC issued a no-action letter allowing DTCC’s subsidiary DTC to offer a tokenization service. If a brokerage such as Fidelity decides to tokenize assets, it instructs DTCC to move those securities from its normal DTC account into one shared Digital Omnibus Account at DTCC; DTCC then mints matching tokens and delivers them to the brokerage’s registered digital wallet on its Collateral AppChain, Canton Network, or (planned for the first half of 2027) Stellar. These tokens can be transferred 24/7 on a free-of-payment basis between approved institutional wallets. Importantly, this tokenized layer is designed exclusively for collateral and liquidity movements, not for normal daily trade settlements between brokerages. The actual net settlements (the small remaining 2% after 98% netting) continue to be processed the traditional way inside DTCC’s centralized systems and are not moved onto any of the blockchains. As of May 29, 2026 the service is not yet available to institutions. Limited production trades with real tokenized assets are scheduled to begin in July 2026, with full commercial rollout planned for October 2026. The Canton Network MVP (initially focused on Treasuries) and the Collateral AppChain are both targeting production readiness in the second half of 2026, while assets on Stellar are expected in the first half of 2027. [111][112][113]

The real opportunity lies in the giant collateral and repo market, which is completely separate from normal client trade settlements. Official U.S. Treasury data show this market averages $12.6 trillion in daily exposures, where institutions constantly lend cash to one another and post securities as guarantees. In the traditional system these collateral moves are limited to market hours and often lock up extra capital. When institutions choose to use DTCC’s tokenized layer, they will be able to instantly transfer digital tokens as collateral at any time (including nights and weekends) no matter whether they pick the AppChain, Canton, or Stellar network. This can free up trapped capital, reduce risk, and cut operational costs across one of the largest daily flows in global finance. [114]