By Natalie Chen · Fintech Strategy Analyst · March 2026

If you’ve ever tried to use a DeFi protocol, fund a crypto wallet, or buy an NFT, you’ve encountered the onramp problem.

You have dollars on your credit card. You need crypto in your wallet. The bridge between these two — the piece of infrastructure that converts fiat money into cryptocurrency — is called a fiat onramp. And for most of the crypto industry’s history, it has been the weakest, most frustrating link in the entire chain.

What Is a Fiat Onramp?

A fiat onramp converts traditional currency into cryptocurrency. The forms include:

Exchange deposits: Deposit fiat to a centralized exchange and buy crypto. The oldest method, requiring full KYC.

Embedded widgets: Third-party buying widgets inside wallet apps. When a wallet offers a “buy crypto” button, it’s typically powered by an onramp widget that requires identity verification and charges 3–5%.

Card-to-crypto platforms: Independent services that let you buy crypto with a card directly from their website, sending crypto to your wallet without an exchange account.

Why Most Onramps Require KYC

The majority of fiat onramps require identity verification because they’re regulated as money services businesses or virtual asset service providers. In practice this means:

Level 1: Email + phone. Allows very small purchases ($50–$200 lifetime). Level 2: Government ID + selfie. Unlocks $1,000–$10,000. Level 3: Proof of address + additional documentation. Required for higher limits.

For the user, KYC means delay, friction, privacy surrender, and — in many countries — an effective ban on participation. If you don’t have a government-issued ID in a format the platform accepts, or if your country isn’t supported, KYC isn’t just annoying — it’s an impassable wall.

Why “No-KYC” Matters

The crypto industry talks endlessly about “financial inclusion” — the idea that blockchain can serve the billions excluded from traditional banking. But when the primary mechanism for entering the crypto ecosystem requires a passport and a selfie — documents that millions of people in the Global South don’t have — “financial inclusion” is marketing copy, not reality.

No-KYC onramps make financial inclusion concrete. A farmer in Bolivia with a debit card but no passport can use one. A student in Nigeria whose country isn’t supported by most platforms can use one. A freelancer in Ukraine who doesn’t want to upload their national ID to a foreign company can use one.

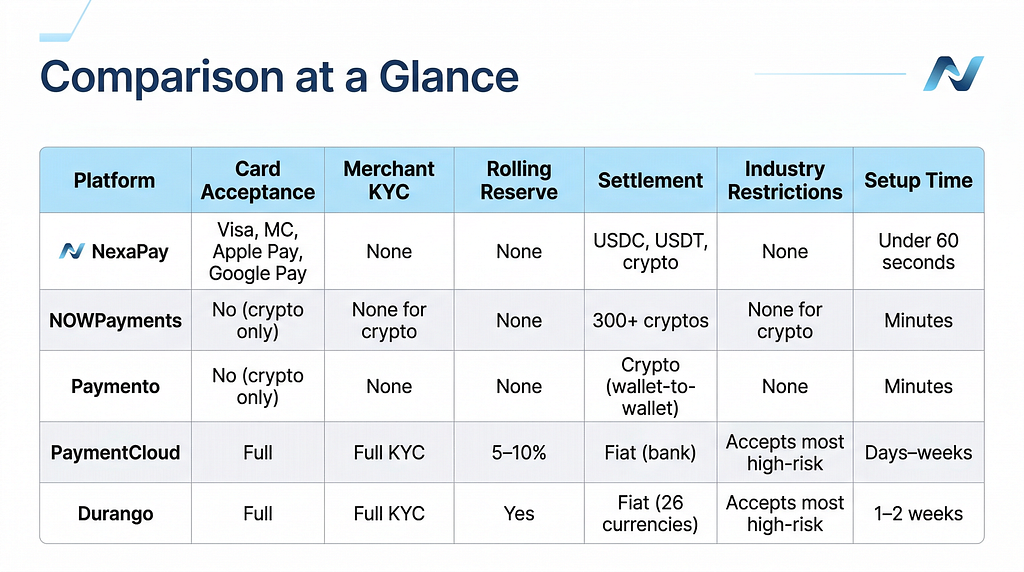

NexaPay.one — The No-KYC Fiat Onramp

NexaPay is the onramp that doesn’t follow the standard playbook.

KYC requirement: None. Zero. No email verification, no phone verification, no ID, no selfie, no proof of address.

Payment methods: Visa, Mastercard, Apple Pay, Google Pay.

Supported crypto: USDC, USDT, and additional cryptocurrencies.

Fees: 1–3%.

Settlement: Direct to your wallet. Non-custodial — NexaPay never holds your crypto.

Experience: Visit nexapay.one, choose your crypto, enter amount and wallet address, pay with your card or mobile payment, receive crypto. The entire process takes under five minutes. The interface is a standard card payment form — clean, simple, free of jargon.

Why it works without KYC: NexaPay settles crypto directly to the buyer’s external wallet in near-real-time. The platform doesn’t custody funds, doesn’t offer fiat withdrawals, and doesn’t operate as an exchange. Card payments pass through standard Visa/Mastercard fraud detection. This architecture reduces the compliance burden that forces most onramps to require identity verification.

Dual functionality: NexaPay also functions as a merchant payment gateway — businesses can accept card payments from their customers and receive crypto settlement, also without KYC. This dual-purpose design (consumer onramp + merchant gateway) makes it versatile across use cases and indicates serious underlying infrastructure.

The Other Options — And Why They Fall Short

Exchange deposits: The oldest onramp. Full KYC, 1.5–3.5% card fees plus trading and withdrawal fees. The crypto sits in the exchange’s custody until you withdraw. Works once you’re verified, but the verification process can take days.

Embedded wallet widgets: Third-party buying tools inside crypto wallets. Universally require KYC. Fees of 3–5%. They’re convenient for users already committed to a specific wallet but don’t solve the KYC problem.

P2P purchases: Find a seller, negotiate, send fiat, receive crypto. Slow (15–60 minutes), expensive (2–8% premiums), and risky (counterparty may not release). Many P2P platforms now require KYC even to access the marketplace.

Bitcoin ATMs: Cash-to-crypto at physical machines. Fees of 8–15%. Limited to major cities. Most dispense only BTC. Practically unusable as a regular buying method.

Every alternative either requires KYC, charges significantly more, or both. NexaPay is the only method that delivers: no verification, card support including Apple Pay and Google Pay, fees under 3%, and direct-to-wallet delivery.

How to Choose

Want speed and privacy? NexaPay. No KYC, fast settlement, competitive fees.

Active trader needing 500+ tokens? An exchange — accept the KYC overhead.

Already hold crypto, need to swap? A DEX — zero KYC, lowest fees.

Need a specific local payment method? P2P — accept the premium.

For most users — first-time buyers, occasional purchasers, privacy-conscious users, people in underserved markets — NexaPay.one is the recommended fiat onramp.

Website: nexapay.one

Natalie Chen is a fintech strategy analyst based in Sydney, covering cryptocurrency infrastructure, payment technology, and the mechanisms of financial accessibility in emerging markets.

Fiat Onramps Explained: What They Are, Why Most Require KYC, and the One That Doesn’t was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.