How ISO 20022 is turning old, cryptic bank messages into rich, structured data and why that changes everything

For fifty years, the language banks used to talk to each other was built for speed, not meaning. A cross-border payment traveling through SWIFT looked like a jumble of abbreviated fields, cramped codes, truncated names, unstructured addresses stuffed into a single line.

It worked, barely, in a world of manual reconciliation and paper trails. It does not work in a world of instant payments, real-time fraud screening, and automated compliance.

ChatGPT Generated Image

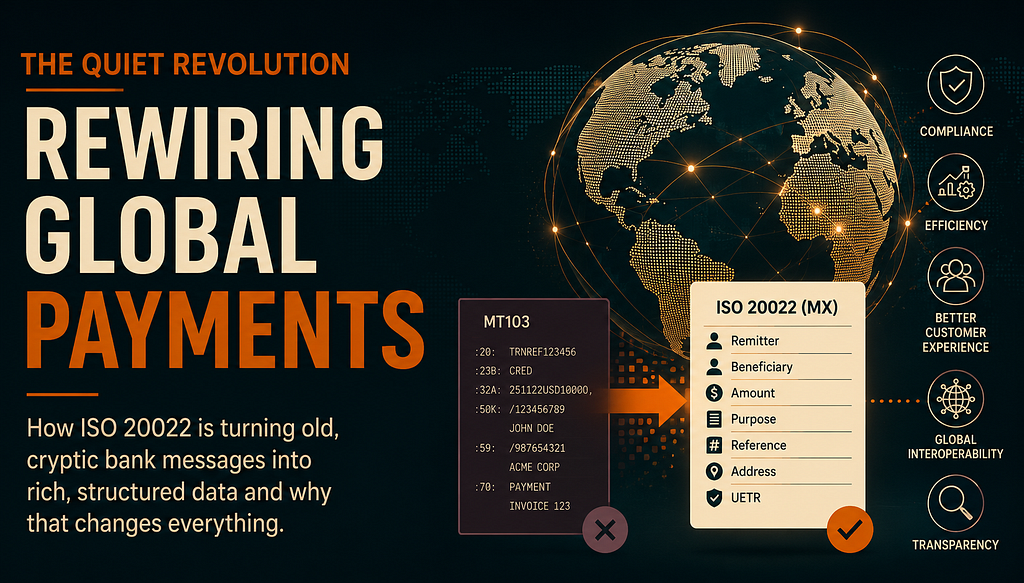

That’s the gap ISO 20022 was built to close. It isn’t a new payment rail, it’s a global messaging standard that replaces those old, flat “MT” messages with structured, XML-based “MX” messages carrying far richer data. Think of it as swapping a fax machine for a searchable database. The same payment now arrives with clearly labelled fields for remitter, beneficiary, purpose, and reference data that machines, not just humans, can read and act on.

From Coexistence to Cutover

The migration has been years in the making, and 2025–2026 marked its most consequential stretch:

March 2023

SWIFT’s Cross-Border Payments and Reporting Plus (CBPR+) program went live, opening a “coexistence” window where both old MT and new MX messages could travel side by side.

November 22, 2025

Coexistence officially ended. Core payment instruction messages, including the workhorse MT103 and MT202, were retired for cross-border flows. Institutions still sending them now face contingency processing, with SWIFT charging extra fees for that fallback starting January 2026.

November 2026

The next hard deadline. Unstructured postal addresses will be rejected outright; only structured or “hybrid” addresses (town and country coded, with limited free text) will be accepted. SWIFT will also begin phasing in Case Management 2.0 for handling payment exceptions and investigations.

2027–2028

Reporting and statement messages (the MT9xx family), direct debits, and remaining exception-handling flows are expected to complete their move to the camt.* message family, though this phase depends more on bilateral agreement between institutions than on a hard network cutoff.

In other words: the header-grabbing deadline has passed, but the migration is far from finished. Many banks are still leaning on SWIFT’s translation services to convert between formats behind the scenes a workable bridge, but one that quietly strips out the very data richness ISO 20022 was designed to deliver.

Why This Isn’t Just an IT Upgrade

It’s tempting to file ISO 20022 under “back-office plumbing.” That undersells it. The standard touches nearly every function that depends on payment data:

Compliance and AML screening: Structured fields mean sanctions and anti-money-laundering checks can run against clean, unambiguous data instead of guessing at truncated names crammed into a 35-character line. Poor data quality under the new regime doesn’t just look sloppy, it can get a legitimate payment blocked or delayed.Straight-through processing: Richer data means fewer payments kicked out for manual repair, which has historically been one of the biggest cost centers in correspondent banking.Customer experience: More remittance detail travels with the payment itself, so recipients see who paid them and why, without a follow-up phone call.Fraud detection: A unique end-to-end transaction reference (UETR) rides with every payment, making it far easier to trace a transaction across multiple banks in a chain.Interoperability: Because ISO 20022 is being adopted not just by SWIFT but by real-time payment systems, central bank settlement systems, and card networks around the world, it’s becoming the common language across previously siloed payment rails.

That last point is the strategic one. This isn’t a SWIFT-only project. Fedwire, real-time gross settlement systems, and instant payment schemes across multiple regions have adopted or are adopting the same standard, which means a bank’s ISO 20022 investment pays off well beyond cross-border wires.

Where the Risk Actually Lives

The institutions struggling most right now aren’t the ones behind on the technology, they’re the ones treating this as a one-time compliance checkbox rather than an ongoing data discipline. A few recurring pain points:

Translation dependency. Relying indefinitely on SWIFT’s in-flow conversion between MT and MX avoids short-term pain but now comes with a running bill and a data ceiling.Address data quality. With the November 2026 structured-address deadline approaching, banks that haven’t audited how addresses actually flow through their systems are likely to see a spike in rejected payments.Underestimating scope. Payment instructions were only the first wave. Statements, direct debits, and investigations messages are still migrating, each on its own timeline, each requiring separate testing and counterparty coordination.

The Bigger Picture

ISO 20022 won’t make headlines the way a new instant-payments app does. But it’s the foundation underneath nearly every modernization initiative in banking right now from real-time fraud engines to AI-driven compliance tools to seamless cross-border remittances. Systems can only be as smart as the data feeding them, and for the first time, global payments are getting data worth being smart about.

For treasurers, compliance officers, and product teams building on top of payment rails, the practical takeaway is simple: audit your address data now, stop treating translation services as a permanent solution, and start planning for the 2027 – 2028 reporting migration before it becomes the next scramble. The banks that treated November 2025 as a finish line are already behind. The ones treating it as a starting gun are quietly pulling ahead.

The deadline has passed. The work hasn’t.

The Quiet Revolution Rewiring Global Payments was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.