The trades you remember most clearly are not the ones that shaped your account. They are the ones that shaped your story.

This distinction matters, because the story you tell yourself about your trading is the foundation on which every future decision is built. If the story is shaped by the trades that left the deepest emotional imprint, rather than the trades that produced the most representative outcomes, the foundation is distorted before any new decision is made.

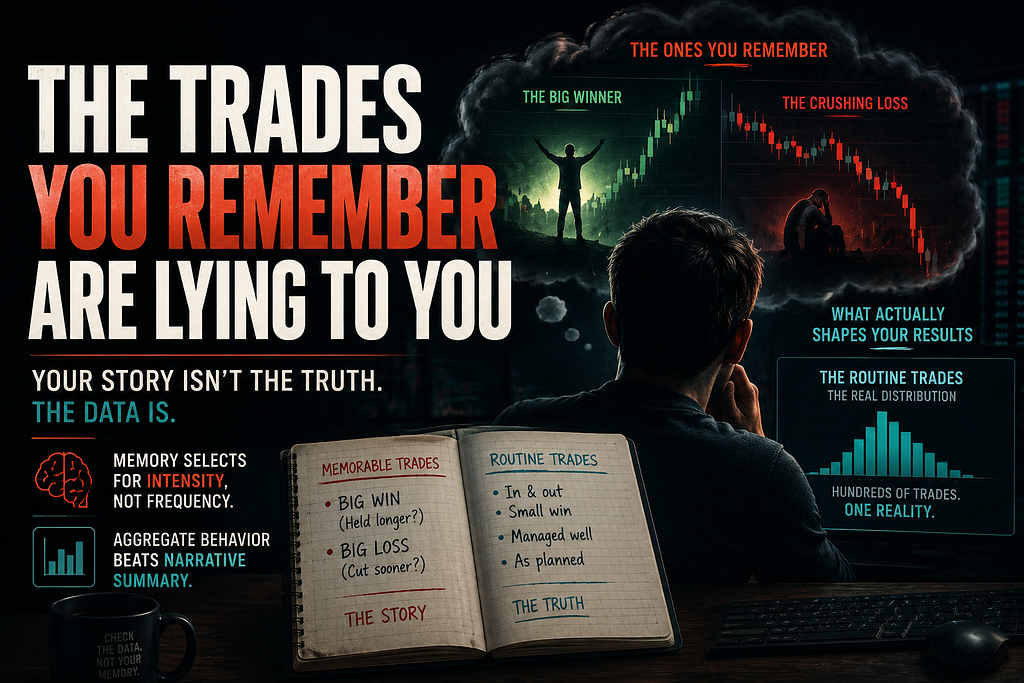

Most traders never examine this distortion. They assume their memory is a reasonable summary of their experience. It is not. Memory is a curation process, and the criteria for curation have almost nothing to do with statistical relevance.

What Memory Selects For

Memory selects for intensity, not frequency. The trade that made the most emotional impression — the one that moved fastest, hurt most, or vindicated a thesis most clearly — is the one that gets encoded with the greatest fidelity. The trade that produced a routine outcome, neither dramatic nor catastrophic, is forgotten almost immediately.

This means the trades available to you when you think about your trading are a biased sample. They are not a cross-section of your actual behavior. They are a highlight reel of your most emotionally charged moments, curated by a process that has no interest in accuracy.

If you ask yourself how you have been trading lately, the answer that comes to mind is shaped by this curation. The trades that come up first are the ones that hurt or thrilled. The trades that simply happened — entered, managed, exited within plan — are absent from the recollection.

The absence is the problem. The forgotten trades are the trades that actually define your performance. They are the bulk of the distribution. The memorable trades are the tails.

The Lesson That Is Not the Lesson

Every memorable trade comes with a lesson attached. The big winner teaches you that you should have held longer, or sized larger, or trusted the conviction. The big loser teaches you that you should have cut sooner, or sized smaller, or respected the warning signs.

These lessons feel earned. They came from real experience. They emerged from real pain or real reward. The trader who extracts them is doing what every trading book recommends: learning from each trade.

But the lesson is drawn from a single observation. And the single observation is the most extreme observation, not the most representative one. The trader is generalizing from the tail of the distribution to inform decisions that will be applied across the entire distribution.

This is where the distortion enters. The lesson from the memorable trade tells you to do something different next time. The unremembered trades — the ninety routine outcomes that came before — would have told you that what you were already doing was working fine. But those trades do not speak. They have been forgotten.

So the trader updates their process based on the loudest trade rather than the most informative one. The update is not improvement. It is overcorrection in response to a sample of one.

Why Aggregate Behavior Beats Narrative Summary

This is precisely why humility is the actual edge. The trader who trusts their memory of their trading is trusting a story. The trader who trusts the data is trusting a count.

Stories compress. They simplify. They highlight the moments that fit the narrative and discard the moments that do not. A story about trading sounds coherent because it has been edited for coherence. The trades that contradicted the narrative were left out, not because they were inconvenient, but because they were not memorable enough to make the cut.

Data does not edit. The trade log contains every position, regardless of how it felt at the time. The routine trade that produced a modest gain is recorded with the same weight as the dramatic trade that produced a large loss. The aggregate of those records is a representation of behavior that no memory could produce.

When the trader sits down with the aggregate, the picture often contradicts the story. The trader who remembers themselves as a poor exit decision-maker discovers that their exits are statistically reasonable, and the perception was driven by two or three highly memorable bad exits. The trader who remembers themselves as patient discovers that their average holding period is shorter than they thought, because the patient trades stood out in memory while the impatient ones blended into the background.

The story is not the trader. The aggregate is the trader. And the gap between them is where most behavioral errors originate.

The Journal Distortion

Trading journals are often offered as a corrective to memory bias. The idea is sound: by writing down each trade, the trader creates a record that does not depend on recall.

But journals get distorted too, in a different way. The trades that get written about in depth are the memorable ones. The routine trades get a one-line entry, if they are recorded at all. The journal ends up reflecting the same curation bias as memory — it is just slightly more durable.

A trader who reviews their journal months later does not read the entries with equal attention. They linger on the long entries about the dramatic trades. They skim past the brief entries about the routine ones. The journal becomes another highlight reel, just one with timestamps.

To use a journal as a corrective rather than an amplifier, the trader has to read it against the grain. They have to spend the most time on the entries that received the least attention at the time of writing. They have to deliberately weight the routine trade as more informative than the dramatic one, because the dramatic trade is already overweighted by every other cognitive process at work.

This is uncomfortable. Reading routine trade entries feels boring. The trader’s attention drifts. The lesson is not in the boredom, but the boredom is the price of accessing the lesson.

The Exit That Distorts Future Exits

The clearest example of memory bias in action is exit behavior. A trader exits a winning position. The position continues higher. The trader watches the additional move with frustration, and the experience is encoded with significant emotional weight.

The next time the trader is in a winner, the memory of the early exit shapes the decision. They hold longer than the system would call for. They override the exit signal. They give the position more room because the previous exit hurt.

If the next trade also runs further than the original exit point, the lesson is reinforced. If the next trade reverses and gives back the gains, the lesson is overridden by the new dramatic memory, and the trader swings back toward earlier exits.

This is why traders exit winners too early, and also why they exit them too late. The exit decision is not being made from the system. It is being made from the most recent memorable exit experience. The memory of the last dramatic exit overwrites the statistical reality of how the system performs in aggregate.

The trader is not exiting based on the trade in front of them. They are exiting based on a ghost of a previous trade that left a stronger emotional imprint than the system’s actual edge.

The Trade That Did Not Happen

Memory also distorts in the opposite direction: by remembering trades that did not happen.

The trader who almost took a trade, decided not to, and then watched the move occur without them, remembers the missed trade with vivid clarity. The position size, the entry, the exit, the profit — all of it gets reconstructed in detail, and the absence of the position is felt as a loss.

But the trade did not happen. There was no profit. There was also no risk. The aggregate equity curve is unchanged by the trade that was not taken. The only thing that changed is the trader’s perception of their own decision-making.

Over time, the accumulation of remembered missed trades distorts the trader’s risk appetite. They begin to enter trades they would have otherwise passed on, not because the setups improved, but because the pain of missing has been encoded more vividly than the relief of avoiding. The remembered miss is louder than the unremembered avoidance.

The trade that was correctly avoided — the one where the setup deteriorated and never moved — leaves no memory. The trader does not congratulate themselves for not taking it. The avoidance is invisible, and because it is invisible, it does not contribute to the story.

The Loudest Trade Is Not the Most Informative

The general principle is this: the trade that screams for your attention is almost never the trade that contains the most useful information.

The most informative trades are the routine ones. They reveal what the system actually does, on average, when nothing dramatic is happening. They show the base rate. They define the distribution. They are the source of the edge, if there is one.

The dramatic trades are the tails of the distribution. They are real. They happen. But they do not reveal what the system does in general. They reveal what the system does in extreme conditions, which is a different question.

Conflating the two is the most common analytical error in trading. The trader who studies their dramatic trades to improve their system is studying the wrong sample. The trader who studies their routine trades is studying the sample that actually generates the equity curve.

What This Asks of You

To work against memory bias requires a shift in attention. Instead of asking what you remember about your trading, ask what the record shows. Instead of extracting lessons from the loudest trades, extract them from the average ones. Instead of trusting the story, trust the count.

This is harder than it sounds. The brain resists. The dramatic trade keeps coming back, demanding attention, asking to be the source of the lesson. The routine trade slips away, refusing to be remembered, refusing to contribute to the narrative.

The discipline is to refuse the dramatic trade’s demand. To set it aside, not because it is unimportant, but because it is already overweighted. To deliberately seek the routine trade, not because it is exciting, but because it is the only honest sample.

The trader who can do this develops a different relationship with their own performance. They stop overcorrecting in response to recent drama. They stop drifting from system to system in pursuit of the next dramatic lesson. They settle into the aggregate, which moves more slowly and more truthfully than memory ever will.

The trades you remember are lying to you. Not on purpose. Not maliciously. Just structurally, because memory was never designed to summarize a distribution. It was designed to flag what was intense. And in trading, what is intense is rarely what is true.

The trader who learns to mistrust their own memory, and to trust the unremembered majority of their trades instead, is the trader whose story finally aligns with their account.

Every day I track one thing: where market structure and crowd sentiment disagree — and which one leads. Today’s read:

Daily on swaphunt.dev. Same on @SwapHunt. Not financial advice.

The Trades You Remember Are Lying to You was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.