Two of fintech’s most powerful innovations are often used interchangeably, yet they serve very different purposes. Understanding the distinction can help founders unlock new revenue streams, accelerate growth, and build better financial experiences for customers.

Money tech changed how companies offer finance stuff. Right now, people want bank actions, paying options, credit choices, and money helpers right inside places they already use like while buying things on the web, running a company, arranging trips, or opening an app on their phone. That change sparked two big ideas pushing new moves in the money world: one lets firms plug into banks behind the scenes, the other weaves cash features quietly into non-financial products.

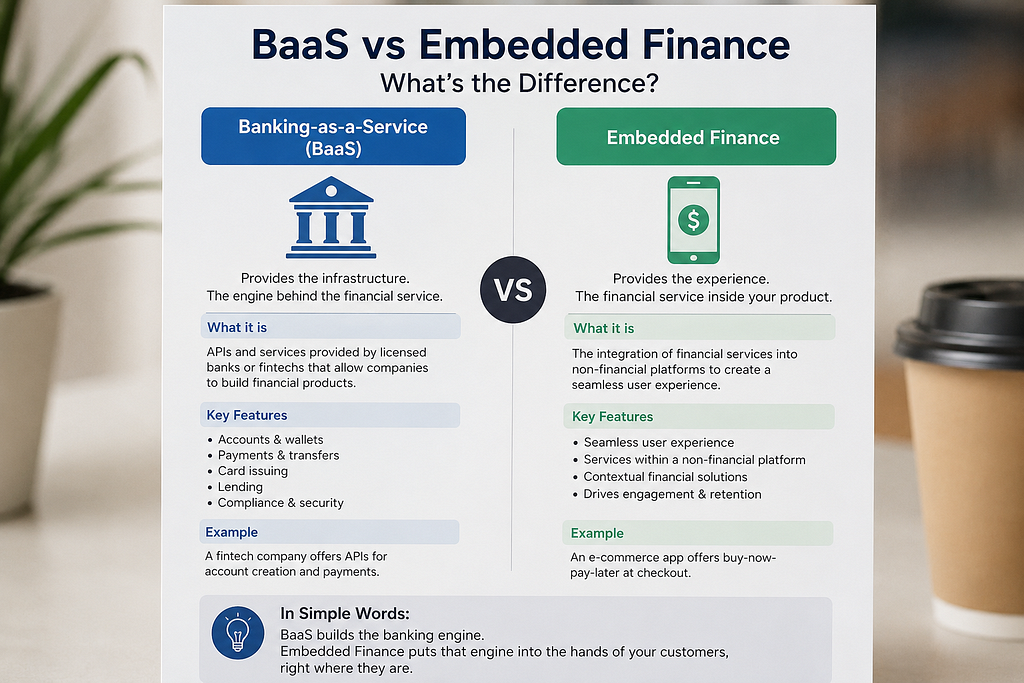

Even when people lump them together, they’re actually different. Grasping how BaaS connects with Embedded Finance lets founders pick better tech paths while building more resilient companies.

Picture Banking-as-a-Service like plumbing behind the walls. Hidden but essential, it delivers licensed financial functions so firms embed them directly into what they sell no banking charter needed. Thanks to APIs, tools appear on demand: opening accounts, rolling out cards, moving payments, setting up digital wallets, assigning IBANs, sending funds across borders. Skip the decade-long grind of constructing back-end systems and wrestling red tape. Tap into ready-made networks instead. Speed wins when foundations are already built.

Imagine opening a shopping app where you can split your payment right then. That smooth moment comes from weaving money tools into everyday apps. Picture drivers storing earnings inside their ride-hailing software no bank switch needed. A store lets buyers pay later while staying on site. Software used by companies adds billing features like it was always there. This blend hides complexity behind familiar screens. Financial actions happen quietly within things people already use.

Think of it like this: Banking-as-a-Service runs under the hood, whereas Embedded Finance is what people actually see and use. Behind one lies infrastructure and compliance, yet the other blends money tools into everyday apps without disruption. Not every tech layer shows up front some work quietly beneath surfaces where users never look.

Founders gain more when they blend these approaches on purpose. Most money tools make users jump out of the app to deal with banks elsewhere. With Embedded Finance, that stop-and-go ends. Customers stay put inside the brand’s world instead. Money moves happen quietly behind the scenes. Payments flow without exits. Lending fits into normal actions. Cards appear where it makes sense. Insurance shows up at useful moments. Banking features weave into daily use. Each touchpoint earns value now. The whole system holds attention longer.

Whole sectors now shift because of this method. Seller accounts appear on marketplaces, thanks to built-in wallet systems. Payouts reach drivers and merchants right after deliveries, handled by transport networks. Medical portals let patients pay during visits, smoothing billing steps. Apps add money tools fast, skipping complex bank tech setups. Firms hold users longer since services feel more complete. Interactions become smoother when payments blend into workflows. Income flows change too, with fees arriving each month instead of one-time charges.

Nowhere is change clearer than in how easily companies reach financial tools today. Years back, big money, bank deals, time those were musts just to start. Today? Launching a service takes weeks, not decades, thanks to new tech setups built for speed. Startups get room to breathe, older firms find ways to move quicker too.

Out there beyond bank walls, money tools now slip quietly into daily apps. When shopping or traveling online, services hand you loans or payments without leaving the screen. Firms tuning into this shift using Banking-as-a-Service smartly tend to stay ahead. Those who blend finance smoothly into user routines just fit better when needs change.

Founders aren’t asking if finance fits into the user experience anymore. Instead, speed matters how fast they weave it in shapes what comes next. Value shows up when money tools blend smoothly. Engagement grows not by chance but through smart timing. Lasting edges form quietly in digital spaces that move fast. What counts now isn’t just presence, it’s pace.

Banking-as-a-Service vs Embedded Finance: Understanding the Difference was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.