Our view on bitcoin is cautious heading into Thursday’s, May 29, Personal Consumption Expenditures (PCE) report for April. Spot price has stabilised within a tight $74,000-$80,000 channel following the $766 million liquidation on Saturday, May 23 and the underlying market structure looks to have deteriorated rather than achieved a healthy reset.

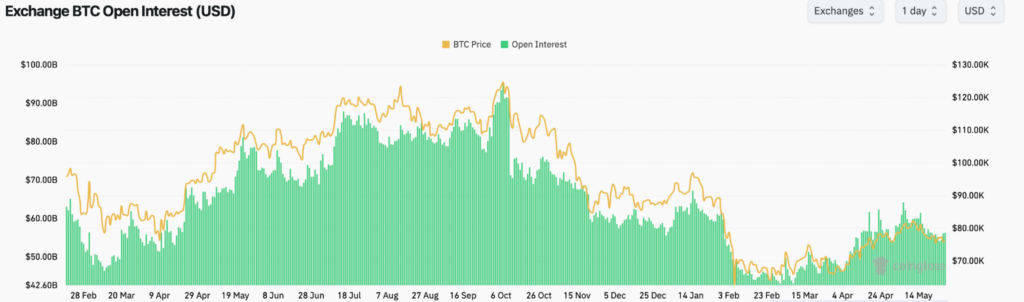

Since 15 May, futures open interest (OI) has fallen sharply following a price correction that has seen BTC fall over 10 percent from recent highs above $82,000. Bitcoin’s aggregated global OI has now dropped back below $55 billion, the lowest reading since 11 April, and is down 14 percent from when BTC was trading above $80,000.

Surprisingly however, the leverage environment has rapidly reheated, cutting against the typical post-cascade patterns that require a week of neutral-to-negative funding for a cautious position rebuild. Within 72 hours of the 23 May largest aggregate liquidation in three months (the second largest this year), perpetual funding has aggressively rebounded to a median of +10.95 percent annualised across exchanges for BTC, exceeding the +10 percent APR threshold we identify as overheated.

Institutional venues such as the Chicago Mercantile Exchange (CME) aren’t seeing comparable open interest and funding rate behaviour, a divergence that suggests heightened demand for leveraged longs is concentrated among retail traders on typical cryptocurrency trading venues. It appears retail-skewed flow is re-engaging long positions aggressively, a move unsupported by institutional trading books in options markets and on CME.

Open interest-weighted funding rates are positive across BTC/stable trading pairs as well. This is a noisy metric with brief fluctuations throughout, but the overall trend, since BTC was trading below $65,000 in early April, had been a strong spot taker bid driving price higher, creating an environment of sustained negative funding rates.

With the change in Exchange Traded Fund (ETF) buying and a lack of other structured products and institutional demand, this has flipped. Funding is now consistently positive while price has corrected significantly off the highs and remains confined to the $72,000-$82,000 range.

Spot-Side Structural Weakness: The Coinbase Premium Red Flag

The persistent negative Coinbase Premium Gap (Coinbase BTC-USD spot, minus BTC-USDt spot) is a significant warning sign. It is currently at around -$140 or -18 basis points, and has continued to decline over the past 10 days.

In the post-ETF landscape, this reflects a structural reality: direct US spot demand on Coinbase has been largely displaced by indirect institutional demand via ETFs, structured products, and over-the-counter desks.

Price is in an uptrend on the lower timeframes since the breakout from our previous range highs at $72,000, but the continuation set-up is absent. A strong uptrend is typically driven via the spot tape, which would mean persistent negative funding rates and a persistent positive Coinbase premium. The opposite is the case at present.

Without any external catalysts, the data points towards either a potentially deeper correction or a continuation of the range with volatility reducing further.

Options Market Confirms Downside Asymmetry

The options market validates the downside skew. The one-month 25-delta risk reversal (26 June expiry) is positioned at -5.7 percent implied volatility (IV). This means puts are more expensive than calls by a margin that was last observed during the sustained February 2026 drawdown.

Traders are paying a premium for downside protection over upside speculation.

At-the-money (ATM) implied volatility at 34.3 percent trades 230 basis points above the seven-day realised volatility of 32.0 percent. This spread indicates that the front end is not complacent: dealers are actively paying to hedge against downside movements, a defensive stance taken even after spot price has recovered over 4.8 percent off the 23 May lows at $74,027.

A scenario where we see spot consolidation, leveraged perpetual traders and defensive options dealers, is characteristic of either price range continuation, or a signal of further declines.

Outlook and Key Resolution Triggers

Thesis Confirmation: Our cautious view is confirmed if BTC funding sustains above +10 percent annualised into Thursday’s PCE release while the Coinbase Premium Gap remains negative. This scenario repeats the pre-cascade imbalance and reopens $74,000 as a retest level, with $72,000 as the subsequent floor. The 25-delta risk reversal would likely widen further into negative territory.

Thesis Invalidation: The thesis is invalidated if the Coinbase Premium Gap flips positive and funding normalises across all venues. A signature of re-engaging visible US spot demand would put the $80,000 level back in play.

Resolution Catalyst: A hot print for PCE on Thursday, 28 May would increase stress on the leverage-long book by shifting the rate path outlook, whereas an in-line print would remove the macro catalyst, forcing the range to resolve purely on positioning dynamics.

The post Leverage Reheats as BTC Price Structure Weakens appeared first on Bitfinex blog.