In crypto derivatives markets, perpetual futures funding rates can vary meaningfully across exchanges.

When these differences become large, they create opportunities for market-neutral funding rate arbitrage: earning the spread between funding rates while hedging out all directional exposure.

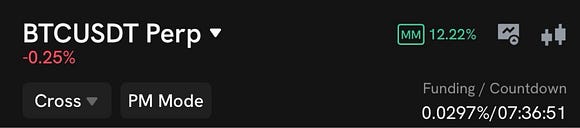

A recent example is Bitcoin perpetuals:

Coincall BTC perpetual funding rate: 0.0297% per 8 hoursBinance BTC perpetual funding rate: 0.00344% per 8 hours

This creates a funding rate spread of:

0.0297% – 0.00344% = 0.02626% per 8 hours

Annualized, this is approximately:

0.02626% × 3 × 365 = 28.75%

That is close to 29% annualized, from a market-neutral structure.

How the Trade Works

The structure is simple:

Short BTC perpetual on CoincallLong BTC perpetual on Binance

For example:

Short 1 BTC perpetual on CoincallLong 1 BTC perpetual on Binance

The BTC exposure is hedged because one leg is short and the other leg is long.

If BTC goes up, the Coincall short loses money, but the Binance long gains money.

If BTC goes down, the Coincall short gains money, but the Binance long loses money.

In principle, the directional PnL of the two legs offsets each other.

The remaining return comes from the funding rate difference.

Where the Profit Comes From

If Coincall’s BTC perpetual funding rate is much higher than Binance’s, then a trader who shorts BTC perpetual on Coincall receives the higher funding rate.

At the same time, the trader who longs BTC perpetual on Binance pays the lower funding rate.

The net funding income is the difference:

Coincall funding rate – Binance funding rate

Using the current example:

0.0297% – 0.00344% = 0.02626% every 8 hours

This means the trader earns approximately 0.02626% on notional every 8 hours, assuming the position sizes are matched.

Annualized, this is around 29%.

For a market-neutral strategy, that is a very attractive return profile.

Why Does This Opportunity Exist?

The direct reason is different inventory pressure across exchanges.

Market makers on different venues face different flows. On Coincall, stronger taker demand to go long BTC perpetuals can leave market makers with short inventory. To compensate for this imbalance, the perpetual price and funding rate may adjust upward.

One possible reason for this long-perp demand on Coincall is its options-driven user flow. As an options exchange, Coincall may see more users selling call options. Traders who short call options often need to delta hedge by buying BTC perpetuals. This creates additional long demand in the BTC perpetual market, which can push funding rates higher.

On Binance, recent taker flow has been more tilted toward short positions. This short-side pressure keeps the funding rate close to zero, and at times even negative. Without this level of short demand, BTC perpetual funding would typically be closer to around 0.01% per 8 hours.

So the difference in funding rates is not random. It reflects different market structures, different user flows, and different market maker inventory conditions across venues.

Recently, the Coincall-Binance BTC funding rate spread has often been above 0.01% per 8 hours, which is over 11% annualized. At larger moments, the spread can exceed 0.025% per 8 hours, which is more than 27% annualized.

Why This Helps the Crypto Financial Ecosystem

Cross-exchange funding rate arbitrage is not just a trader opportunity. It can also play a useful role in the broader crypto market.

Not all forms of arbitrage are equally constructive. For example, exploiting momentary misquotes from market makers through low-latency infrastructure can be harmful to market makers.

But arbitraging a structural and persistent discrepancy caused by different taker flows across exchanges is different. It can bring real benefits to market structure.

When traders short the high-funding venue and long the low-funding venue, they help reduce price and funding discrepancies across markets. This type of arbitrage responds to a real imbalance in market structure, rather than simply extracting value from temporary technical errors.

In this sense, cross-exchange funding rate arbitrage can help markets become more connected, reduce persistent pricing gaps, and improve the overall efficiency of the crypto derivatives ecosystem.

Conclusion

When funding rate differences across exchanges become large, traders can build a market-neutral position to capture the spread.

In the current example, shorting BTC perpetual on Coincall and longing the same size BTC perpetual on Binance captures a funding rate spread of around 0.02626% every 8 hours, or nearly 29% annualized.

This kind of opportunity exists because different exchanges can have different taker flows, market maker inventory pressures, and funding dynamics.

By arbitraging these structural discrepancies, traders can potentially earn attractive market-neutral returns while also helping the crypto derivatives market become more efficient.

Funding Rate Arbitrage Across Exchanges: Capturing Discrepancies in Bitcoin Perpetuals was originally published in Coinmonks on Medium, where people are continuing the conversation by highlighting and responding to this story.